Yesterday, MEPC’s post focused on unemployment and jobs in Mississippi. In keeping with the theme of assessing where Mississippi is 50 years after the March on Washington, today’s post focuses on access to affordable banking services. Having a relationship with a depository institution is incredibly important. In families where a parent has a bank account, a child will be more likely to save and gain knowledge on the ways to build assets than a child from a family that does not have a bank account. Additionally, children with savings are more likely to “expect” to go to college and “progress” once enrolled. Finally, households without a bank account are more likely to use high cost financial services.

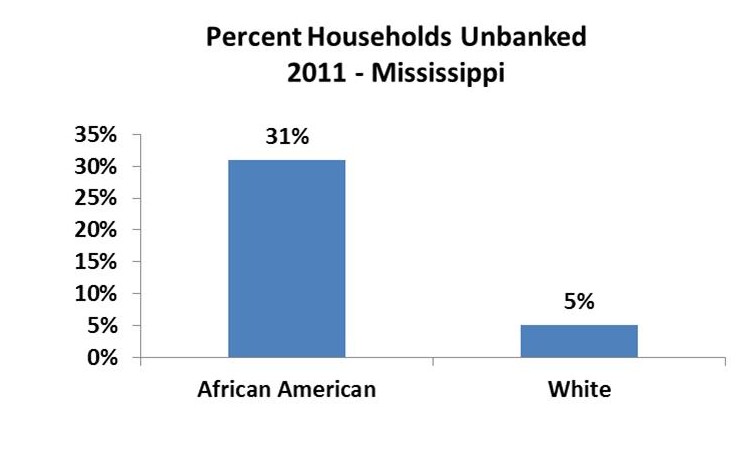

Despite the clear benefits of having a relationship with a bank, quite large disparities exist in bank account ownership in Mississippi by race. The chart illustrates the gap.

In Mississippi, nearly one out of three African American households is unbanked compared to only 1 out of 20 white households. The gap in account ownership is quite a bit larger than the gap across the United States. Nationally, 21% of African American households are unbanked compared to only 4% of white households. Reasons identified for being unbanked include a perception of not having enough money, a perception of not needing an account and a lack of trust in banks.

Given the benefits of account ownership, Mississippi will not be able to realize its full economic potential if such a large portion of its population remains disconnected from the banking system. Investments in community development activities and institutions, such as credit unions, that increase access to affordable financial services are needed to connect more households to a regulated financial institution. Additionally, policies (such as strengthening the Community Reinvestment Act) that create incentives for banks to serve low-income communities and disincentives for banks to leave low-income communities are also necessary to ensure that any family that wants to have a banking relationship can have one.