Consumer Financial Protection Bureau: Know Before You Owe

September 9th, 2016

The 2008 financial crisis and subsequent Great Recession had widespread consequences on many American households – unemployment skyrocketed, millions were stripped of their wealth, and the housing “bubble” burst. The deep effects of unemployment, household wealth, and to the housing markets are still very much felt today, particularly in the Mid South, as families and communities continue to recover. As a way to prevent the reoccurrence of another financial crisis, the Dodd-Frank Wall Street Reform and Consumer Protect Act of 2010 became law to bring accountability and transparency to our nation’s financial system.

A component of the law includes the Consumer Financial Protection Bureau (CFPB), which “aims to make consumer financial markets work for consumers, responsible providers, and the economy as a whole.” Since its establishment, the CFPB has made significant progress to promote fair, transparent, and competitive markets. Among its many achievements is the “Know Before You Owe” initiative, focused on redesigning the materials people use to make decisions about mortgages, student loans, and credit cards.

A Closer Look: “Know Before You Owe” Mortgages

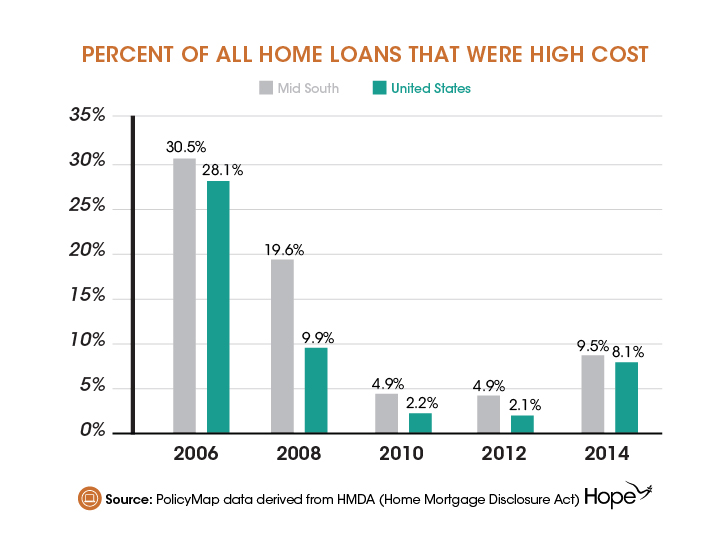

The “Know Before You Owe” mortgage disclosure rule, or TILA-RESPA Integrated Disclosures (TRID), was created after the housing crisis (see chart for an example of impact) to help consumers better understand their loan options and to help prevent costly surprises at the closing table.

Historically, consumers shopping for a mortgage received two redundant disclosure forms that explained the final terms and costs of the loans: the initial Truth-in-Lending disclosure with the Good Faith Estimate and the final Truth-in-Lending disclosure with the HUD-1 Settlement Statement. These lengthy forms were filled with complicated terms thought to make the process harder for the borrower to understand and for lenders to explain.

The CFPB acknowledged the need to streamline this information for consumers and replaced the two forms with the “Know Before You Owe” disclosure forms, intended to help consumers better understand their loan options, choose the deal that is best for them, and to avoid costly surprises at the closing table.

To see how the CFPB improved the disclosures, see here.

The CFPB works with the intent to protect consumers. After the housing crisis, the CFPB created the “Know Before You Owe” mortgage disclosure rule to not only make the process easier for consumers but to also make sure that financial institutions and mortgage lenders that consumers depend on every day continue to operate fairly and efficiently.

For more information on the “Know Before You Owe” initiative and other consumer resources, visit www.consumerfinance.gov or to submit a complaint with a financial product or service, visit www.consumerfinance.gov/complaint/.

Share this article.