FDIC Survey: South has Highest Rates of Unbanked and Underbanked

September 17th, 2012

People who have an account with a bank or credit union are better positioned to participate in the economy and contribute to the nation’s recovery. A relationship with a financial institution enables individuals to more securely plan for future investments as they work their way toward financial stability.

Banks and credit unions allow people to save their income build assets to purchase a home, start a business, or further their education. However, a large number of American households do not have access to basic financial tools like checking and savings accounts.

According to the 2011 FDIC National Survey of Unbanked and Underbanked Households, more than one in four households (28.3 percent) are either unbanked or underbanked.

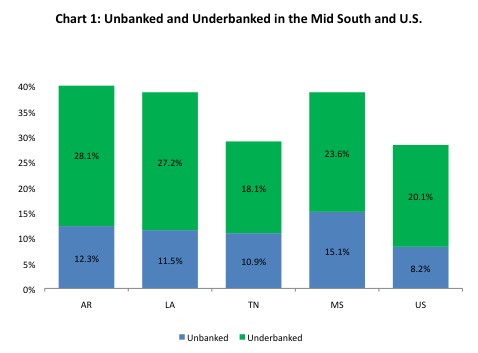

Unbanked – have no checking or savings account.

In the United States, nearly 10 million households (8.2 percent) are unbanked. Mississippi has the highest percentage of unbanked households in the country, followed by Texas and Arkansas. Approximately 173,000 households (15.1 percent) in Mississippi are unbanked. See Chart 1.

Underbanked – have an account but continue to depend on costly alternative financial services for basic transactions and credit needs, like check cashers, payday loan providers, pawn shops, auto title lenders and rent-to-own stores. These businesses charge high fees for their services – services that deplete rather than preserve income and wealth.

In the U.S., approximately 24 million households (20.1 percent) are underbanked. Mississippi has 269,000 underbanked households (23.6 percent). Compared to the rest of the nation, Arkansas and Louisiana have the third and fourth highest rate of underbanked residents in the country. See Chart 1.

Unbanked and underbanked households typically operate in a cash-based system, and, as a result, do not have the same financial security and opportunities as those who bank with traditional financial institutions. The unbanked and underbanked are more likely to spend a percentage of their net income on unnecessary fees. They are also more likely to be victims of crime, because they often carry their cash or keep cash in their homes.

The new data underscore the importance of implementing policies that promote financial inclusion. When households are attached to the financial mainstream, they have the tools available to save and build wealth as well as the opportunity to pass good financial habits onto children.

Interestingly, the states with the highest rates of unbanked populations are those states with large immigrant and African American populations. Given the shifting demographics of the country, pursuing policies that support successful models of connecting households of color to the financial mainstream remains essential to maximizing opportunity in America. Examples of those policies include expanding support for community development finance institutions and community development credit unions to continue the work of meeting the needs of historically underserved populations.

Source: FDIC, 2011 FDIC National Survey of Unbanked and Underbanked Households, 2012.

Share this article.