Findings from the Survey of Household Economics and Decision Making – Part 1

June 24th, 2022

By Kiyadh Burt, Vice President of Policy & Advocacy and Interim Director

In May, the Federal Reserve Board released findings from its annual Survey of Household Economics and Decision Making. Commonly referred to as the SHED report, the publication provides insights into the overall “economic well-being” of households in the United States. Importantly, the survey synthesizes data collected by race and income which allows one to measure disparities across a variety of financial indicators. Also of note, data were collected in October / November of 2021 and reflect sentiments of households in the fall. Over the next two blogs, we will highlight high-level findings. This first dive into the SHED report spotlights banking, credit and housing outcomes.

Banking and Credit Access

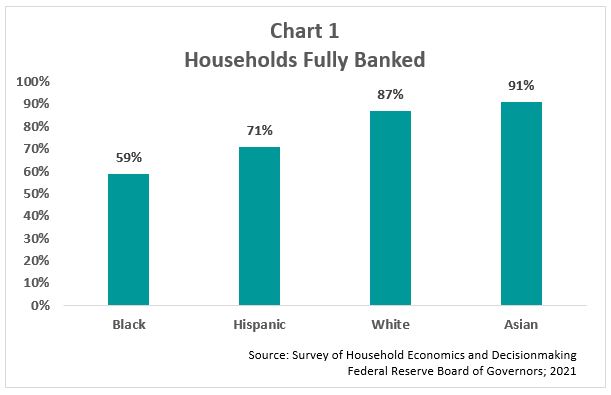

Longstanding disparities in banking access continued to persist in 2021. The percentage of Black and Hispanic households reporting being fully banked lagged significantly behind white and Asian households (Chart 1).

Racial disparities were also very evident in credit access. Whereas 43% of white households earning less than $50,000 reported being denied credit or receiving less than requested, 60% of Black households with the same characteristics reported this experience. Even among households earning over $100,000, more than one out of five Black households did not receive what was requested, in contrast to only 8% of white households. Another finding focused on credit card access and use. Over 70% of all racial and ethnic groups owned a credit card, however, carrying a balance varied greatly. While one out of four Asian households and less than half of white households carried a credit card balance, nearly 3 out of 4 Black households – well above all other groups – carried a balance from month to month.

Housing

Homeownership rates were highest among white and Asian households, while Black and Hispanic households reported rates well behind their white and Asian peers. Relatedly, Black households were more than twice as likely to rent as white households. One in five Black and Hispanic renters also reported being behind on rent in 2021 – up from pre-pandemic levels and well above their white and Asian counterparts. One reason for the gaps included an increased likelihood of layoffs for Black and Hispanic renters working in sectors at risk of contraction in response to the economic conditions created by the virus outbreak.

Looking Ahead

Gaps in banking and credit access are best addressed through increased investment in historically underserved communities and the institutions that expand financial service access. Community Development Financial Institutions (CDFIs) and Minority Depository Institutions (MDIs) with long track records of success serving people and communities of color represent a proven approach for advancing this goal. Long term, sustained efforts to capitalize MDIs are vital to ensuring MDIs remain a viable option for people systemically overlooked by the banking sector – particularly in the Deep South.

Share this article.