New Report Examines Racial Disparities in the Mortgage Market

July 31st, 2012

A new report from the Paying More for the American Dream collaborative shows evidence of a two-tiered mortgage market. “Paying More for the American Dream IV: Racial Disparities in FHA/VA Lending” is a collaborative report that examines geographic discrimination in the mortgage market. The authors of the report analyzed 2010 Home Mortgage Disclosure Act (HMDA) data and compared conventional and government-backed mortgage lending based on the race and ethnicity of borrowers and communities in seven cities throughout the United States – Boston, Charlotte, Chicago, Cleveland, Los Angeles, New York City, and Rochester.

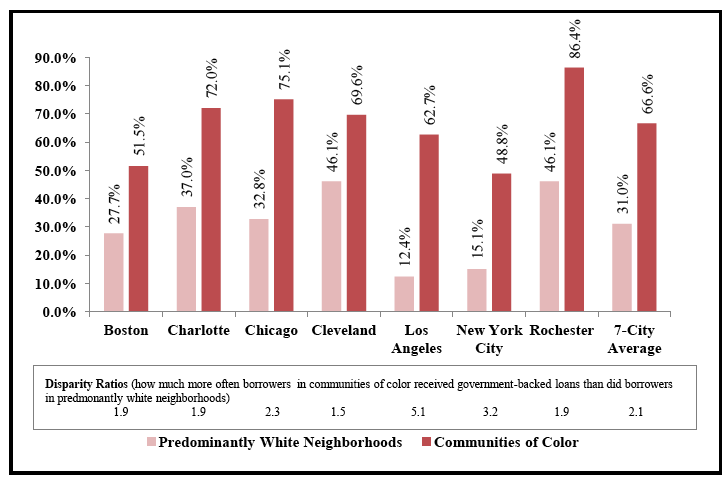

The report found that African American and Latino borrowers and borrowers in communities of color received more government-backed loans, particularly Federal Housing Administration (FHA) and Department of Veterans Affairs (VA) loans, than did Caucasian borrowers and borrowers in white communities. In all seven cities examined, the majority of home-purchase mortgage loans in communities of color were government-backed (see Chart 1). Essentially, the authors found that borrowers and communities of color received disproportionately fewer conventional mortgages and disproportionately more government-backed mortgages than did white borrowers and communities. As such, the authors believe that there is a segregated mortgage market, which raises two major issues: the issue of possible mortgage redlining and the issue of racial loan steering.

Chart 1: Prevalence of Government-Backed Home-Purchase Loans in Predominantly White Communities and Communities of Color

Based on the racial disparities found in the report, the authors believe major changes to the mortgage lending system are needed. They provided the following recommendations:

- Regulators must ensure access to affordable mortgage loans for people and communities of color;

- The Community Reinvestment Act (CRA) must be expanded and enforced to promote responsible lending and investment;

- Fair lending enforcement must be a top priority for all;

- Governments must require servicers, trustees, and holders of foreclosed properties accountable for maintaining the properties; and

- HMDA data enhancements must be promptly implemented at the loan level to allow identification of possible lending discrimination.

Although banks are making conventional loans, the report’s analysis indicates their provision of conventional credit is far more restricted to people of color and in communities of color. In addition to insuring fair lending among traditional banks, solutions to addressing disparities in home lending should include efforts to capitalize Community Development Financial Institutions and low-income Community Development Credit Unions – institutions that have a long track record of providing affordable and sustainable mortgage lending products to historically underserved populations.

Source: Woodstock Institute. (2012, July). Paying more for the American dream VI: Racial Disparities in FHA/VA Lending. Retrieved from http://www.woodstockinst.org/blog/blog/report%3a-fha%10va-lending-concentrated-in-neighborhoods-of-color/

Share this article.