Scorecard: Financial Security in Mississippi

January 30th, 2014

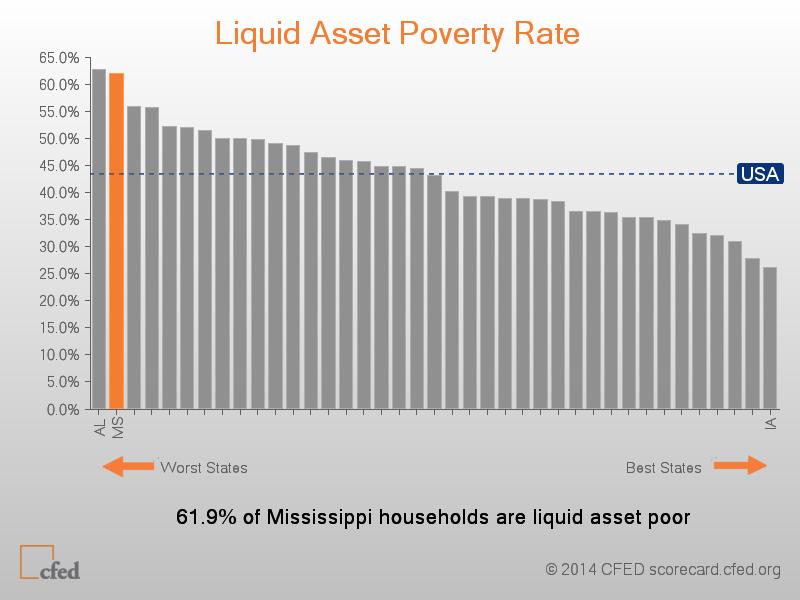

Today, the Corporation for Enterprise Development (CFED) released its 2014 Assets & Opportunity Scorecard, which comprehensively examines the ability of residents to achieve financial security in all 50 states and the District of Columbia, and, for the first time, policies designed to help them get there. The 2014 Scorecarde evidences a serious problem for households today – while some progress has been made to ensure financial security, a growing number (43.5 percent) of American families are “liquid asset poor,” meaning they lack the means to meet their expenses for three months should a job loss or other emergency leave them without their primary source of income. In Mississippi, 61.9 percent of residents live in liquid asset poverty. See Chart.

Today, the Corporation for Enterprise Development (CFED) released its 2014 Assets & Opportunity Scorecard, which comprehensively examines the ability of residents to achieve financial security in all 50 states and the District of Columbia, and, for the first time, policies designed to help them get there. The 2014 Scorecarde evidences a serious problem for households today – while some progress has been made to ensure financial security, a growing number (43.5 percent) of American families are “liquid asset poor,” meaning they lack the means to meet their expenses for three months should a job loss or other emergency leave them without their primary source of income. In Mississippi, 61.9 percent of residents live in liquid asset poverty. See Chart.

In addition to this troubling statistic, the Scorecard ranks each state and the District of Columbia on 66 different outcome measures. Some of the clearest areas of improvement for Mississippi include income poverty, unbanked households and consumers with subprime credit, where the state has the worst rates in the nation. However, there are several bright spots for the state. For instance, both unemployment and foreclosure rates improved from last year. Mississippi also has the 8th lowest level of credit card debt, with an average of $6,837 per borrower.

Although our state does not perform well in each category, that is not to suggest that there are not clear, manageable steps we can take to improve the financial opportunities afforded to families across the state. For example, to reduce high income and asset poverty and improve credit scores, Mississippi can adopt tax credits so low-income families have more income to pay down debt and save. The state can also implement policies that promote lifelong savings through Children’s Savings Accounts. To protect unbanked and underbanked households from predatory financial products, Mississippi can implement enhanced consumer protections around a number of alternative financial services.

Over the next several months, MEPC will be sharing information about the Scorecard and promoting policy options for building assets among low-wealth families.

Source: Corporation for Enterprise Development, Assets and Opportunity Scorecard, 2014.

Share this article.