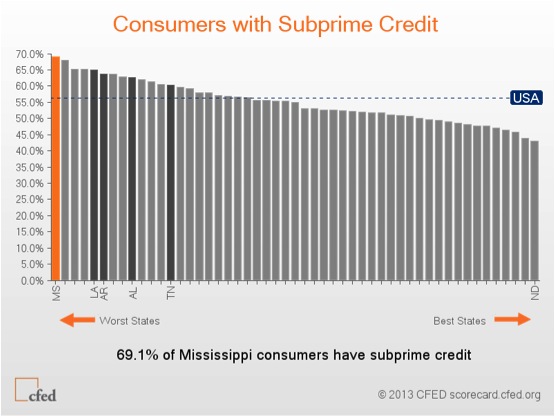

Three-digit credit scores are largely based on a consumer’s financial history and ability to pay bills in a timely manner. Likewise, credit scores help determine the extent to which a borrower can finance higher education, own a home or purchase a vehicle. The CFED defines consumers with subprime credit as the “percentage of consumers with a TransUnion TransRisk Score at or below 700 (on a scale of 150-934).” Consumers with subprime credit have a more difficult time securing credit from a traditional financial institution or lender and often pay higher interest rates on loans. In the United States, 56.4 percent of consumers have subprime credit, while 69.1 percent of consumers in Mississippi have subprime credit. Compared to the rest of the nation, Louisiana and Arkansas have the fifth and sixth highest percentage of consumers with subprime credit, respectively. See Chart.

Consumers with weak credit scores oftentimes lack access to mainstream credit and rely on high-cost, predatory lenders. This makes it increasingly more difficult for consumers with subprime credit to invest in wealth-building opportunities like higher education or homeownership. Additionally, studies have shown a consistent disparity between the credit scores of white and black consumers – less than a quarter of blacks have prime credit, compared to approximately 65 percent of whites. Interestingly, the states with the highest percentage of consumers with subprime credit are also states with large African American populations.

The data underscore the importance of implementing policies that promote access to the financial mainstream, so more consumers have the appropriate tools needed to save and build wealth for future investments. Furthermore, it is particularly important to pursue policies that support models of connecting households of color – households that are more vulnerable to a financial crisis or loss of income – to the financial mainstream. Examples of such policies include expanding support for Community Development Financial Institutions (CDFIs) and Community Development Credit Unions (CDCUs) to continue the work of meeting the needs of historically underserved populations

Sources: Corporation for Enterprise Development. (2013). Assets and Opportunity Scorecard, 2013. Retrieved from http://assetsandopportunity.org/scorecard/ Mui, Y. (2012, July 8). For black Americans, financial damage from subprime implosion is likely to last. The Washington Post. Retrieved from http://www.washingtonpost.com/business/economy/for-black-americans-financial-damage-from-subprime-implosions-is-likely-to-last/2012/07/08/gJQAwNmzWW_story.html