Student Loans: Women More Likely to Struggle to Repay

March 29th, 2017

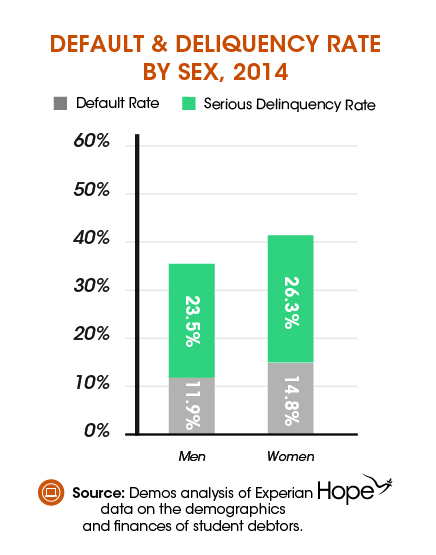

Women student debtors – and especially women of color – are more likely to experience the negative financial consequences associated with student loan delinquency and default. According to one of the three major credit rating bureaus in the United States, women borrowers are more likely to be in default on their student loans or in serious delinquency than men (Figure 1).

Click to enlarge

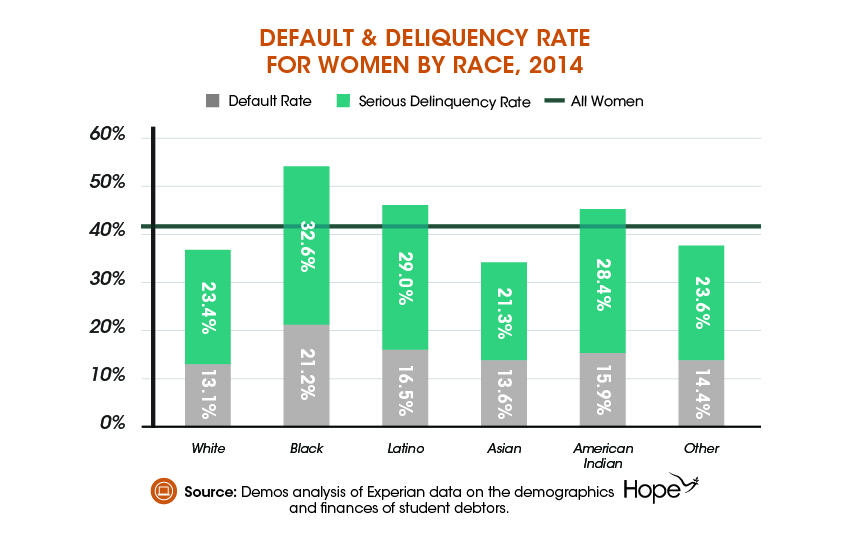

Debtors in default have not made payments on their loans in over 270 days (approximately nine months), while debtors in serious delinquency have not made payments in over 90 days. Student debtors in these two groups are called “distressed borrowers.” Nationally, four in ten (41.1 percent) women borrowers are in serious delinquency or default. Rates among women of color are often even higher. Black women have the highest rates of distress with over half (53.8 percent) of borrowers responsible for loans in either serious delinquency or default (Figure 2).

Click to enlarge

Failing to repay student loans on-time every month levies serious financial consequences. Distressed borrowers struggling to make regular payments can expect their credit scores to drop. Consumers with weak credit can expect to pay higher interest rates on credit cards, car loans, and mortgages and to have greater difficulty getting approved.

Factors that influence the ability of women borrowers to repay student loans are unclear. Women represent a larger portion of higher education students, which could explain why a larger number of distressed borrowers are women. Alternatively, women are frequently paid less than males in the workplace, regardless of educational attainment, which could potentially impact their ability to repay when loans come due. Whatever the cause, the burden of student loan debt means borrowers have limited ability to juggle additional financial concerns in both the short- and long-term. Investments that build assets and increase economic security, like retirement fund contributions or a down-payment on a house, could be out of reach for the many women borrowers already under the onus of student loan delinquency or default.

The calculations for this blog were generated by Demos from a data set on the demographics and finances of student debtors obtained from Experian. The data set was created from the credit records of 35,000 student debtors, sampled from Experian’s entire credit database in December 2014.

Share this article.