The Honorable Jelena McWilliams

Chairman

Federal Deposit Insurance Corporation

1776 F Street, NW

Washington, DC 20006

Submitted via email to comments@fdic.gov

Re: Comments on FDIC Notice of Proposed Rulemaking, Federal Interest Rate Authority, 12 CFR Part 331, RIN-3064-AF21

Dear Chairman McWilliams,

Please find below the comments of the Hope Enterprise Corporation / Hope Credit Union (HOPE) in response to the FDIC Notice of Proposed Rulemaking, Federal Interest Rate Authority, 12 CFR Part 331, RIN-3064-AF21.

HOPE is a credit union, community development financial institution and policy institute that provides affordable financial services; leverages private, public and philanthropic resources; and engages in policy analysis to fulfill its mission of strengthening communities, building assets, and improving lives in economically distressed areas throughout Alabama, Arkansas, Louisiana, Mississippi and Tennessee. Over the last 25 years, HOPE has generated over $2 billion in financing that has benefited more than one million individuals.

Given the experiences of our members, described herein, we are concerned that the FDIC proposals will add to, rather than relieve, the burdens of high-cost lending in our region. In four of the five states in our footprint, high-cost lenders, such as payday and car title lenders, are already saturating our communities. For example, in 2017 in Tennessee, there were over 1,200 payday loan storefronts, more than McDonald’s and Walmart locations combined.1

In terms of fees drained by payday and car title lenders, Mississippi, Alabama, Louisiana, and Tennessee are in the top ten states, and high-cost lenders drain more than $1.6 billion every year from low-income borrowers in these four states.2

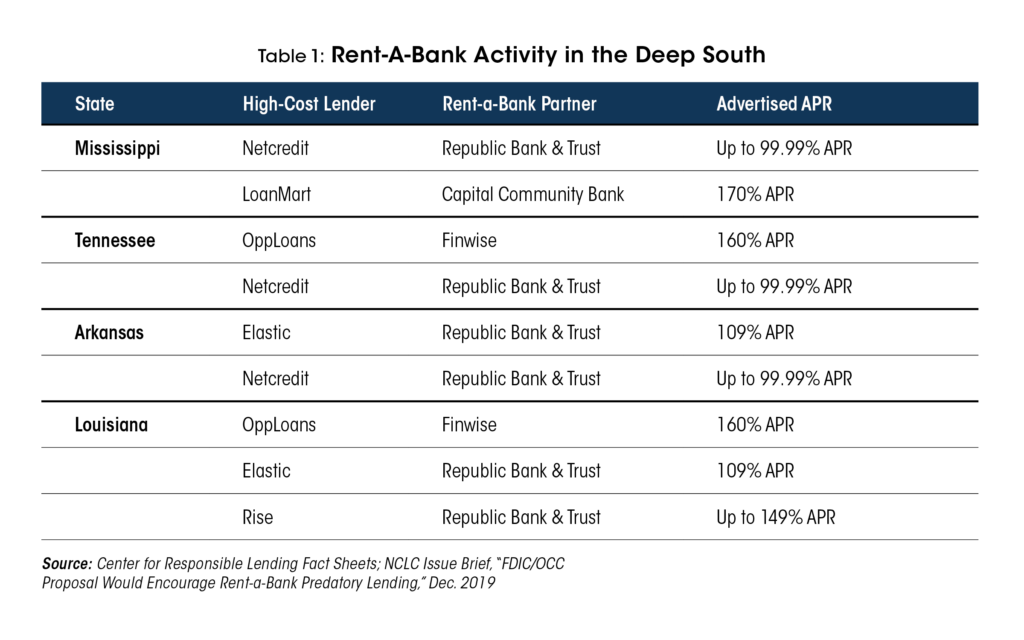

In four states in our region, there are at least two high-cost lenders making these loans via the bank partnership arrangement. (Table 1) The FDIC proposal increases the risks that more high-cost lenders will extract additional fees, aided by the willing assistance of partnering banks.

We recognize that to date, these arrangements involve only FDIC-supervised banks. We are disappointed that FDIC has not taken steps to rein in these existing arrangements, and rather has chosen to issue this proposal which will encourage more lenders to engage in high cost lending.3

The Proposal Exacerbates the Harms Experienced by HOPE’s Members

HOPE’s concerns about the harms of these loans are not hypothetical. HOPE members have been trapped by loans facilitated by rent-a-bank partnerships, putting their economic success in jeopardy and thus frustrating our mission to build wealth among low-income communities and communities of color in the Deep South. People are not being harmed by the absence of the loans supported by the FDIC proposal; rather, it is the presence of additional high-loan cost loans that is the problem. If promulgated by this rule, the expansion of these high-cost loan products will further exacerbate the financial strain of low-income borrowers in the Deep South.

Over the course of the fourth quarter of last year, 60 HOPE members had at least one loan from either Elastic, Rise, OppLoans, or NetCredit via the rent-a-bank arrangement. This is a concerning number. The greatest concentration of members, 86%, stuck in rent-a-bank loans, are in the three states that already allow storefront payday lending (TN, MS, LA). People stuck in the rent-a-bank loans are people on fixed incomes receiving social security or disability benefits, veterans, students, teachers, and workers at hospitals, fast food places, and even payday loan shops.

From our members’ experiences, at least three key themes of harmful lending practices emerge:

- Despite claims to the contrary, rent-a-bank loans are going to people who already have credit. People with rent-a-bank loans have other types of consumer credit outstanding at the same time, often at much lower costs than those charged by rent-a-bank lenders. As one example of a frequent pattern, one borrower had several outstanding consumer loans and credit cards, in addition to the high-cost rent-a-bank loans.

- Rent-a-bank loans are deepening people’s financial burdens, not relieving them. Where a borrower has a rent-a-bank loan, the payments are in addition to existing outstanding debt, or in some cases contribute to the need to take out additional loans after receiving the rent-abank loan. For example, one of HOPE’s members, a disabled veteran on a fixed income, received a rent-a-bank loan in July. By December, he had also taken out an additional online payday loan, now owing on both. For another member, at the beginning of the year, the payments on four outstanding consumer loans, inclusive of a high-cost rent-a-bank loan, accounted for 32% of her monthly take home pay. By the end of the year, she was still making payments on all four debts plus two new additional loans, such that the payments now accounted for 60% of her monthly take home pay.

- There is a clear disregard for a borrowers’ ability to repay. The disregard for a borrowers’ ability to repay is evident in two ways. First, by the time a borrower receives a rent-a-bank loan, many times he or she has additional loans outstanding, including ones on which he or she was struggling to repay. One of HOPE’s members found herself in this situation. After missing two previous payments on an existing lower-cost consumer loan she received a high-cost rent-a-bank loan just days later. Second, there is evidence of clear patterns of repeat re-borrowing, both through repeated cycles throughout the year, and multiple refinances by a single lender over a short period of time. Another member of HOPE’s refinanced a loan originated by the same rent-a-bank lender twice within six-months of receiving the loan, with payments increasing each time. This cycle mirrors that which is so well-documented in the context of payday lending — where one finds it nearly impossible to both repay the loan and meet other monthly obligations without re-borrowing.

These harms are neither exclusive nor exhaustive. We hear first-hand from our members and people in the communities where our branches are located about the troubles caused by unaffordable high-cost loans, such as difficulty paying other bills, the psychological stress caused by unaffordable debt, and the subsequent inability to build wealth in the future.

Beyond HOPE members, research shows that high-cost loans, even when structured with longer-terms and over installments, can have devastating effects on people’s financial situation.

Such harms are, in part, why the U.S. Department of Defense extended its 36% rate cap to cover high-cost installment loans, in addition to the short-term loans that were previously covered.4 Empirical data from states with high-cost installment loans similar to those being made in our region through these rent-a-bank partnerships still show troubling patterns of repeat re-borrowing and other burdens like difficulty meeting other obligations.5

The Proposals Puts State Law Consumer Protections at Risk

The FDIC proposal will put at risk the consumer protections that currently exist in our region, particularly the 17% constitutional rate cap in Arkansas.6

Did you know?

The proposals encourage lenders to circumvent this rate cap which saves Arkansans $139 million a year in fees that would otherwise be drained by high-cost lenders.7

The benefits of Arkansas’s law are documented in a recent report about how borrowers are faring several years after the enforcement of the rate cap.8 As one person said, they are doing “[m]uch better financially. You don’t continue to repeat the vicious cycle.”9

Beyond Arkansas, other state law protections in our region are at risk, such as but not limited to, Louisiana’s rate cap for consumer installment loans.10 In recent years, payday lenders and highcost lenders have made attempts to move legislation that would undue these caps in Arkansas and Louisiana, but thankfully, these efforts have failed to gather the support needed by the respective state legislatures to come to fruition. The FDIC must not override the policy decisions of the states as it is doing with this proposal.

These devastating financial consequences of loans made via this rent-a-bank arrangements would be troubling for anyone, but they are particularly pronounced in the Deep South, where economic inequality is deeply entrenched and persistent poverty is prevalent. The five states of our region all have higher rates of unbanked and underbanked populations than the national average.11 The high-cost loans that will occur through the FDIC proposal will only serve to increase these rates as people are exposed to practices that ultimately damage their financial standing.

In light of these concerns, HOPE urges the FDIC to withdraw its proposal.

Sincerely,

William J. Bynum

Chief Executive Officer

Footnotes

- Metro Ideas Project, “Fighting Predatory Lending in Tennessee,” 2017 https://metroideas.org/projects/fightingpredatory-lending-in-tennessee/ ↩︎

- Center for Responsible Lending, “Payday and Car-Title Lenders Drain Nearly $8 Billion in Fees Every Year,” April 2019, https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-statebystatefee-drain-apr2019.pdf ↩︎

- JDSupra, “OCC and FDIC file joint amicus brief urging Colorado federal district court to reject Madden,” Sept. 12, 2019, https://www.jdsupra.com/legalnews/occ-and-fdic-file-joint-amicus-brief-64121/ ↩︎

- See e.g., National Consumer Law Center, “Misaligned Incentives: Why High-Rate Installment Lenders Want Borrowers Who Will Default,” July 21, 2016, https://www.nclc.org/issues/misaligned-incentives.html ↩︎

- U.S. Department of Defense, Press Release, “Department of Defense Issues Final Military Lending Act Rule,” July 21, 2015, https://www.defense.gov/Newsroom/Releases/Release/Article/612795/department-of-defense-issues-finalmilitary-lending-act-rule/ ↩︎

- Arkansas Constitution of 1874 Amendment 89, 3. Maximum interest rate on other loans. https://codes.findlaw.com/ar/arkansas-constitution-of-1874/ar-const-amend-89-sect-3.html ↩︎

- Center for Responsible Lending, “Shark‐Free Waters: States are Better Off without Payday Lending,” April 2019, https://www.responsiblelending.org/research-publication/shark-free-waters-states-are-better-without-payday-lending ↩︎

- Southern Bancorp, “Into the Light: A Survey of Arkansas Borrowers Seven Years after State Supreme Court Bans Usurious Payday Lending Rates,” May 2, 2016, https://banksouthern.com/sbcp/into-the-light/ ↩︎

- Ibid., ↩︎

- La. Rev. Stat. Ann. §§ 9:3510 to 9:3568 ↩︎

- According to the Prosperity Now Scorecard, 26.9% of people in the U.S. are unbanked or underbanked, which is lower than the states of Mississippi (38.1%), Louisiana (37.8%), Alabama (36.4%), Arkansas (32.3%), and Tennessee (30.0%). ↩︎