Every day in its work, HOPE hears stories of people and families facing financial pressure as the cost of everyday household expenses continue to mount. New data from the Urban Institute’s American Affordability Tracker help paint a stark picture of this reality for the country and for the Deep South, showing data for a range of economic metrics over time. This blog uses the Tracker tool to analyze economic conditions across HOPE’s footprint and compare them to national trends, with a focus on wages, the cost of essential expenses, loan delinquencies, and credit scores.

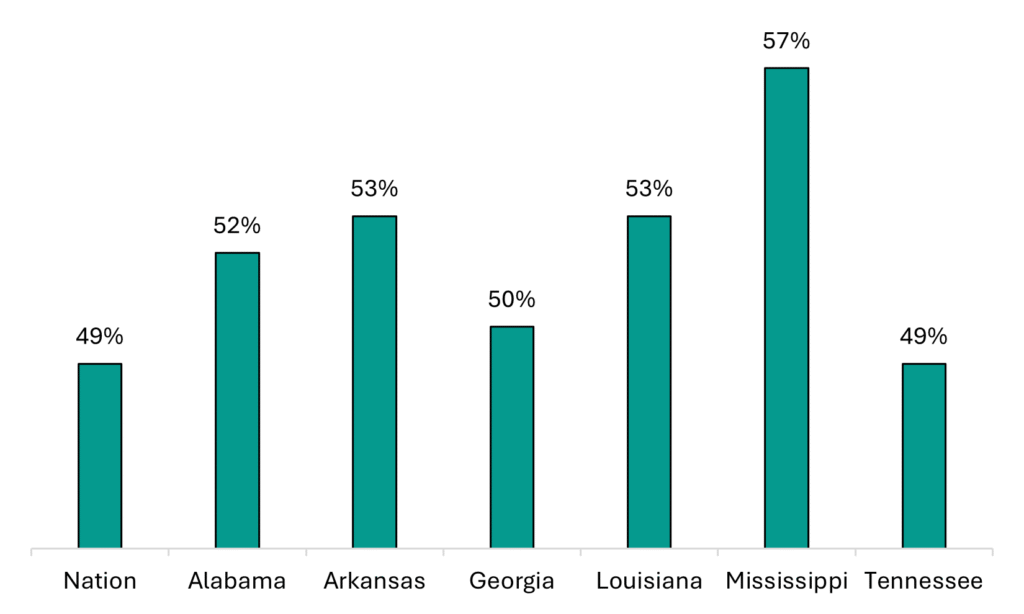

According to the Urban Institute’s data, nearly 1 in 2 households are unable to fully participate in today’s economy, nationally.1 For every state in HOPE’s footprint, it is the same or an even higher share of households. See Figure 1. At 57%, Mississippi has the highest rate in the country of households without full economic participation.

These gaps in national and Deep South rates reflect deeper, more persistent challenges tied to regional economic conditions and longstanding inequities. The ongoing affordability crisis and subsequent financial stress may further exacerbate this gap, dragging both individual economic stability and economic opportunity for the region.

Figure 1: Percent of Households Unable to Fully Participate in Economy

Flat Incomes, Rising Costs

Across much of the Deep South, incomes have remained stagnant while the costs of everyday life continue to climb. For example, according to the Affordability Tracker, the average price for a gallon of gas in Mississippi has spiked in recent months. Gas prices have jumped from an average of $2.33 in February 2026 to $3.43 by the end of March, with similar trends in Louisiana as gas prices rose from $2.42 to $3.51 during that time.

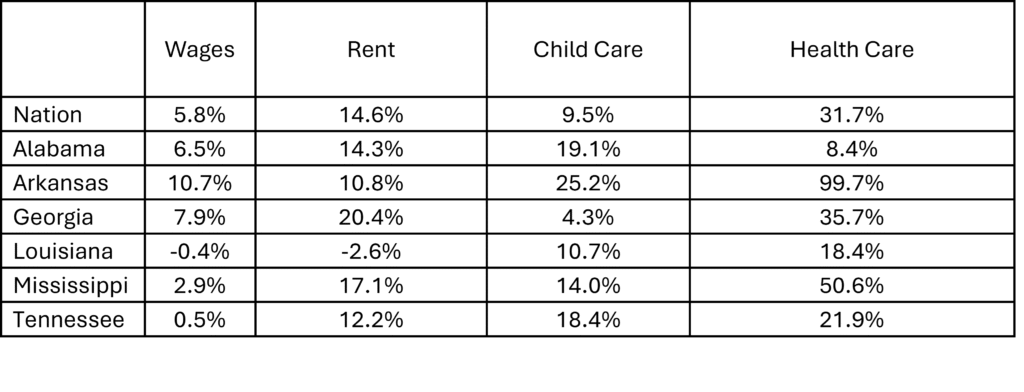

When looking back over the last decade, for many households, wages have not kept pace with essential household expenses such as housing, childcare, and healthcare. See Table 1. Compared with the national average, Deep South states generally experienced higher increases in healthcare and childcare costs than elsewhere. Even though in three Deep South stages wages increased at a higher rate than nationally, they still lag behind increases in expenses in their states.

Table 1: Percent Increase Comparison between Average Monthly Wages and Monthly Household Expenses, 2017-20262

Arkansas illustrates the intensity of this affordability crisis. Between 2017 and 2026, the state experienced the highest rate of average wage growth in the region (10.7%), which is double that of the nation (5.8%). During the same time, however, childcare expenses jumped by 25% and average healthcare costs have essentially doubled, even when counting for inflation. The impact of higher earnings is blunted by the more acute increases in household expenses. Higher earnings alone are not enough. Louisiana demonstrates another challenge with declining wages combined with higher childcare and healthcare costs.

In a region of the country where people already have less financial cushion than elsewhere, these trends indicate that many households may face greater difficulty weathering the shocks of these increased expenses. Ultimately, this makes it even harder to manage existing debt or to even save for the future.

Financial Strain Leads to High Delinquencies

As costs rise, financial strain is increasingly visible in household balance sheets. Delinquency rates across the Deep South are among the highest in the nation, with several Deep South states leading in missed payments on student loans, auto loans, and mortgages.

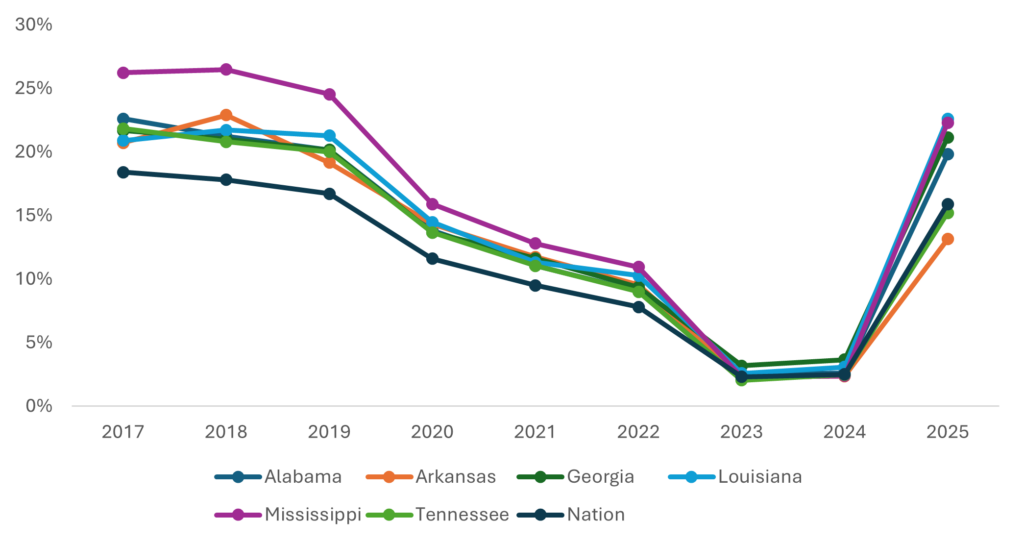

Figure 2: Student Loan Delinquency in Deep South, 2017-2025

Households in the Deep South consistently experience higher student loan delinquency rates than the national average.3 See Figure 2. Delinquency rates show a downward trend even before the pandemic-era borrower relief efforts; however, households are now facing renewed financial strain as repayments resume and relief programs phase out. Consequently, delinquency rates since 2024 have increased sharply to pre-pandemic levels almost instantly, indicating that borrowers are experiencing acute financial stress but now with less federal support and the added impact of stagnant wages and increased costs.

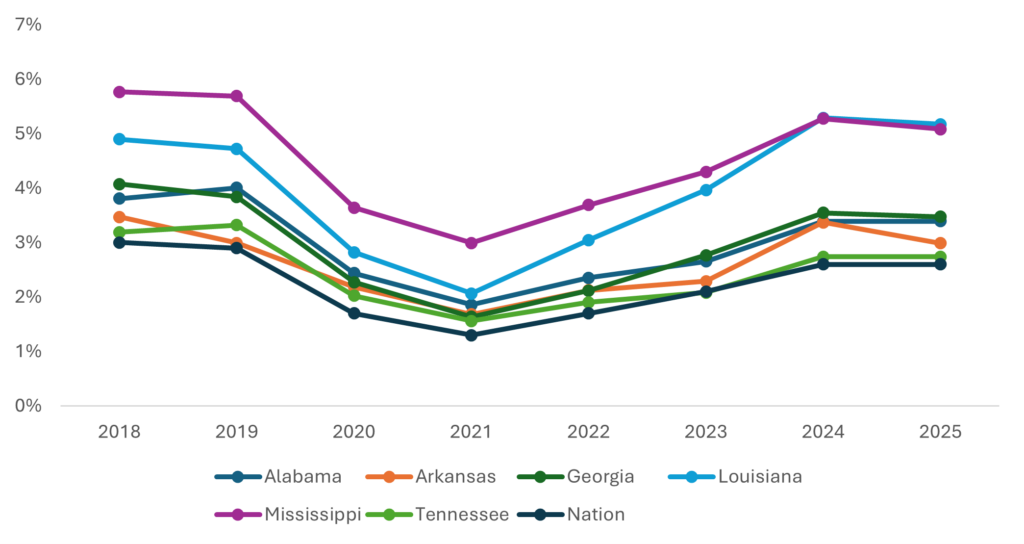

Figure 3: Auto and Retail Delinquency in Deep South, 2017-2025

Similarly, Deep South states consistently exceed national delinquency rates for auto and retail loans. Mississippi shows the highest and fastest-growing delinquency rates, exceeding 10% by 2025. The increasing financial strain on households’ ability to manage everyday expenses, such as auto and retail debt, is often associated with borrower stress in other financial areas such as struggling to pay their mortgage or other bills.4 As these delinquencies rise, households have less liquidity and limited financial buffers which may lead to vehicle repossession or job loss, deepening economic instability across the region.

Figure 4: Mortgage Delinquency in Deep South, 2018-2025

Mortgage delinquency rates in the Deep South, while lower than other loan types, are rising and consistently exceed the national average. Mississippi and Louisiana exhibit the highest levels and fastest increases in mortgage delinquencies in the region. This upward trend signals growing risks to housing stability and homeownership, particularly as households face escalating homeowners’ insurance costs and property tax burdens.

Delinquencies Undermine Credit and Opportunity

When households fall behind on debt, the consequences continue beyond a missed payment. Delinquencies damage credit scores, making it harder to qualify for affordable loans, secure housing, refinance debt, or recover financially. For example, data by the Federal Reserve show that newly delinquent student loan borrowers are experiencing drops in their credit scores, between 100 and 150 points, pushing many borrowers below the threshold for affordable credit access.5

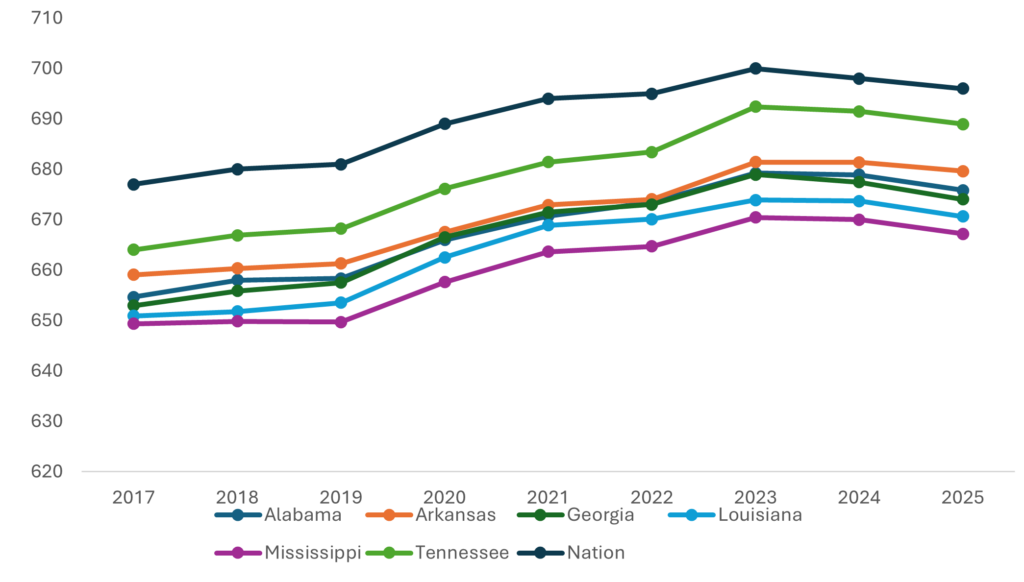

Across the Deep South, average credit scores remain consistently below the national average. In the region and nationally, credit scores peaked in 2023, but have been on the decline, coinciding with the end of pandemic-era relief programs and rising costs since that time. As such, with credit score declines, the current affordability crisis may scar people’s financial records in such a way that will continue to make life more expensive for people well into the future.

Figure 5: Average Credit Scores in Deep South and the Nation, 2017-2025

As wages fail to keep pace with rising costs, families, especially households in the Deep South, are forced to make difficult tradeoffs that can lead to debt, damaged credit, and reduced pathways to wealth-building through homeownership or savings. Without intentional action, these gaps will continue to widen and deepen regional inequities.

Policymakers, financial institutions, and community leaders must respond with solutions that lower the cost burden on working families, expand access to safe and affordable credit, and invest in the long-term financial stability of Deep South communities. Increasing the number of people and families who can fully participate in the economy drives opportunity both for the region and for the nation as whole.

Footnotes

- The Urban Institute defines this as the True Cost of Economic Security, which measures “the total cost of goods and services necessary to fully participate in today’s economy and society and save money for emergencies and the future.” See more at, https://www.urban.org/data-tools/american-affordability-tracker?metric=tces_rate_all ↩︎

- These increases are calculated using dollar amounts adjusted for inflation. The childcare data is based on the cost of two children in childcare from 2017 to 2024, the most recent data available. ↩︎

- Student loan delinquency is defined here as the share of student loan holders whose loans are 60 days or more past due or in default, using a nationally representative data set of consumer-level credit records from a major credit bureau. ↩︎

- See e.g., Consumer Financial Protection Bureau, “Consumer Finances in the Rural South,” at 27 https://files.consumerfinance.gov/f/documents/cfpb_or-data-point_consumer-finances-in-rural-south_2023-06.pdf (finding that from 2020 to 2022, for borrowers in the rural South who were delinquent on their auto loan, 20% were also delinquent on their mortgage and nearly 60% delinquent on their credit card.) ↩︎

- Andrew Haughwout, et al, “Student Loan Delinquencies are Back and Credit Scores Take a Tumble, Liberty Street Economics, May 13, 2025, https://libertystreeteconomics.newyorkfed.org/2025/05/student-loan-delinquencies-are-back-and-credit-scores-take-a-tumble/ (defining newly delinquent borrowers as student loan borrowers that were current on their student loans in the fourth quarter of 2024 but had at least one student loan that was ninety or more days past due in the first quarter of 2025) ↩︎