The State Small Business Credit Initiative (SSBCI) has been re-authorized with the passage of the American Rescue Plan.

States will receive a portion of the $10 billion allocation to offer flexible relief programs for businesses in need with some key provisions, which includes a $1.5 billion set aside for socially and economically disadvantaged businesses.

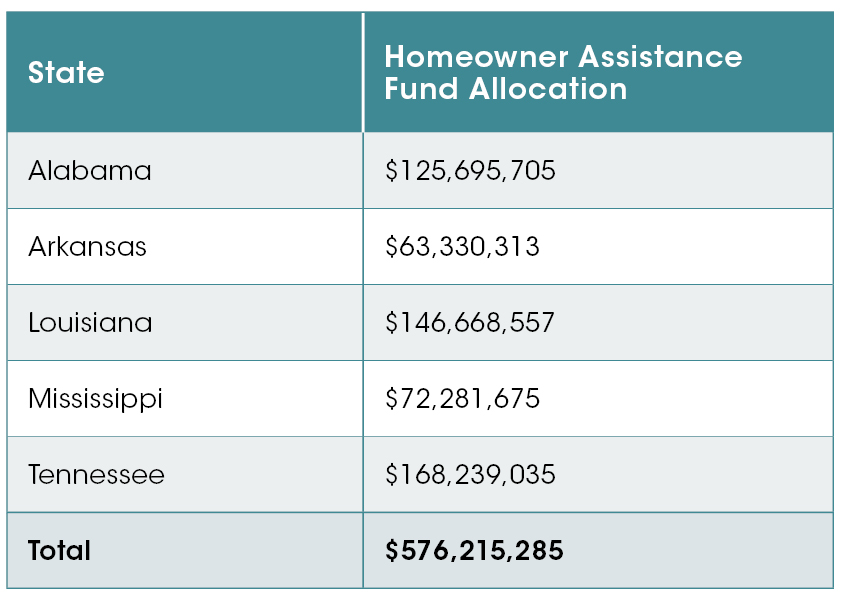

With six times more funding this round than the original SSBCI program in 2010, states will have more capital to create much needed programs to spur business growth and survival. Deep South states are set to receive $308 million in funding, which is a three fold increase from the previous round.1 See Table 1.

Table 1: 2021 Deep South SSBCI Allocations

SSBCI represents an opportunity to address inequities in access to capital and to strengthen relationships between state governments and community development financial institutions (CDFIs) and minority depository institutions (MDIs). To that end, we provide an overview of SSBCI, review Deep South states’ SSBCI lending impact, and raise recommendations on how best to ensure funds flow to underserved businesses, particularly those in rural persistent poverty communities and businesses owned by people of color.

Overview of SSBCI

SSBCI is a federal program administered by the U.S. Department of Treasury to support small businesses. It allows states, territories, and eligible municipalities the opportunity to expand existing small business programs or to create new ones through public private financing. States have the authority to design and implement programs as well as the ability to determine underwriting and operating procedures. Most state economic development agencies administer the SSBCI programs, which generally are categorized as loan guarantees, venture capital, collateral support, loan participations, or capital access programs. States partner with eligible lenders e.g. banks, credit unions, community development financial institutions (CDFIs)—to deploy funds with the goal of obtaining a 10:1 leverage ratio where for every one dollar of SSBCI funds, 10 dollars of private financing is generated. This means, in the Deep South, the $308 million allocation has the potential to unlock more than $3 billion in small business capital.

Originally, SSBCI was authorized with a $1.5 billion allocation in response to the Great Recession. The program lasted from 2010-2017, and Treasury reports that SSBCI funds supported more than 21,000 loans, totaling over $10.7 billion, with more than 80% of the funds and investments made to small businesses with 10 or fewer full-time employees. These funds helped small businesses create or retain over 240,000 jobs (240,669).2 Community banks, midsized banks, and CDFIs facilitated the majority of SSBCI support loans (94%).3

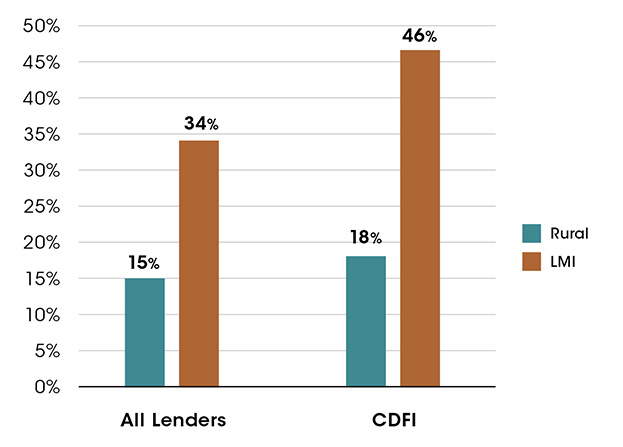

However, not all communities benefitted from SSBCI funds equitably. Only 15% of all SSBCI funds from 2010 to 2017 went to rural communities. Comparatively, CDFIs slightly performed better in rural lending with 18% of funds going to rural communities and on par with non-CDFI lenders (19%). In terms of reach into low- and moderate income communities, 34% of total SSBCI funds were directed to businesses located in low to moderate income areas. CDFIs, again, performed better with 46% of lending directed to businesses in low- to moderate income areas as compared to 32% for non-CDFI lenders.4 See Chart 1. Treasury did not report on the extent to which these funds went to communities or borrowers of color. In this next round, Treasury and Deep South states have to opportunity to ensure a more equitable distribution of this critical capital resources.

Chart 1: SSBCI Lending To Target Areas

There is great flexibility with small business program design but typically, SSBCI programs are in one of the following categories:

- Capital access programs – lender and borrower contribute a percentage of the loan amount into a portfolio loan loss reserve in the case of loan default. Contributions are matched dollar for dollar with SSBCI funds.

- Loan guarantee programs – states guarantee or assure up to 80% of loan in the case the loan defaults. The lender guarantees whatever the state does not.

- Collateral support programs – states provide cash to lenders to help cover collateral shortfalls.

- Loan participation programs – states use SSBCI funds to make direct loans to borrowers and pair with private loans (companion loans), or purchase a portion of loans originated by lenders to borrowers. In the case of a companion loan, state funds will be subordinate to lender’s senior loan.

- Venture capital programs – states purchase ownership interest or provide equity–like loans to startups or other high-risk enterprises.

Review of Deep South Impact

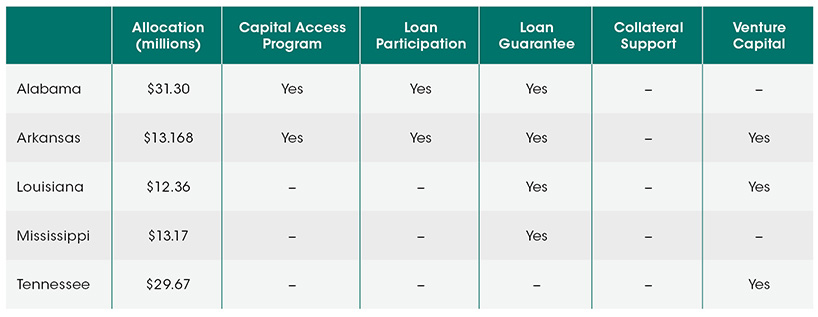

In the 2010 SSBCI Program, the Department of Treasury allocated $99.6 million in SSBCI funds to Deep South state financial development authorities. Deep South states, like many other program participants, created loan guarantee programs and venture capital programs, and to a lesser extent capital access and loan participation programs. The most popular relief program in the Deep South was the loan guarantee program. Interestingly, no state created a collateral support program. See Table 2. States with a wider variety of program offerings tended to be more successful in the reach and deployment of their funds.

Table 2: Deep South SSBCI Allocations and Programs, 2010-2017

Lending to distressed areas, particularly low-income and rural communities varied greatly.

Did you know?

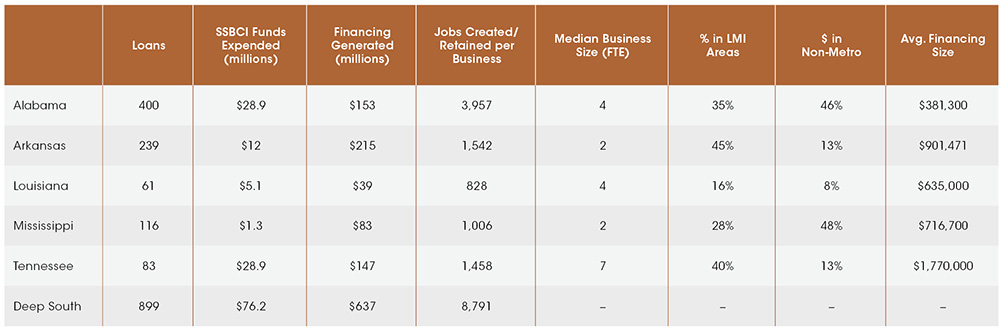

Alabama and Mississippi lead the Deep South in lending to rural communities with 46% and 48% of loans, respectively, to businesses located in non-metro areas, which was much better than the national lending rate of just 15%.5

Arkansas and Tennessee trailed with 13% of loans to businesses in rural areas with Louisiana showing the least levels of lending to rural businesses at only 8% of its loans. See Table 3. Looking at just the rural lending data alone can be misleading in terms of assessing reach to underserved or disadvantaged businesses. For example, in Mississippi, despite nearly 50% of loans going to rural businesses, only 28% of loans were directed to businesses in low-income areas in the state. The majority of loans went to larger agriculture businesses.

Table 3: Deep South SSBCI Lending Impact

Not all Deep South states meaningfully engaged CDFIs and MDIs in the process. As one promising example, United Bank, a CDFI in Alabama, deployed over a third of loans in Alabama’s loan guarantee program, which represented the bulk of the state’s loans to low to moderate-income areas.

Policy Recommendations

Given the disparities in lending to rural and low- to moderate-income communities in the Deep South and of the overall program, we suggest the following recommendations to ensure disadvantaged communities are better served during this round of SSBCI.

- Leverage the Expertise and Infrastructure of CDFIs/MDIs with Strong Track Record of Reaching Underserved Communities, Disadvantaged Businesses and Very Small Businesses

- Without a statutory requirement for States to provide a CDFI/MDI engagement plan, not all states will engage these specialized lenders in a meaningful manner. Treasury should use all available tools to move states to meaningfully engage with CDFIs/MDIs serving their states, particularly those with a track record in reached underserved and disadvantaged communities and businesses. States should engage CDFIs/MDIs throughout the application process, to include input on front-end program design, as well as form partnerships such as several states did last round in which CDFIs/MDIs directly administered portions of the SSBCI funds.

- Allow and Encourage CDFIs and MDIs to Administer Portions of State SSBCI Funds Directly to Ensure Funds Reach Underserved Communities, Disadvantaged Businesses, and Very Small Businesses

- Given the track record of CDFIs and MDIs in serving disadvantaged businesses, CDFIs (including nonprofit loan funds, credit unions, and banks) and MDIs should be considered eligible lenders or administrators for any state program funded by SSBCI funds. In addition, Treasury guidance should highlight CDFIs/MDIs’ unique ability to meet statutory requirements to serve underserved communities, particularly socially and economically disadvantaged businesses and small businesses in persistent poverty areas.

- CDFIs and MDIs should not simply serve as administrators of the fund, but should also retain SSBCI funds as capital. Retaining the SSBCI capital on their balance sheets is extraordinarily valuable to a CDFIs/MDIs, as it enables the CDFI/MDI to amplify its reach to underserved businesses. It also creates the opportunity for SSBCI funds to revolve, further stimulating lending, providing more capital for businesses, and increasing SSBCI’s impact in underserved communities over time.

- Ensure Funds Are Directed to Distressed Communities through Data Collection

- Treasury should require states to collect and publish race and gender data of the borrowers benefitting from the program to ensure programs are reaching underserved communities, as well as minority-owned and women-owned businesses. As demonstrated by the state-level CARES Act programs, states are already collecting such data from businesses receiving support through federal relief dollars. The failure to collect such data, as shown by the Paycheck Protection Program, leaves gaping holes in understanding the demographics of who benefited from these funds.

- Treasury should also require data collection to assess the geographic distribution of the businesses served. During the previous round of SSBCI, states provided thorough data on the rate at which SSBCI funds were directed to businesses in Low to Moderate Income and non-metro areas. This round, Treasury should also report data on the businesses supported in counties that are designated as persistent poverty counties and counties in which the majority of residents are people of color.

For a more detailed discussion of these and other recommendations, see the Partners for Rural Transformation’s recommendations to U.S. Treasury for ensuring SSBCI funds reach persistent poverty communities.

SSBCI is an opportunity for states to increase access to transformative capital for businesses that have been disproportionately impacted by the pandemic and historically locked out of emergency response programs. As policymakers incorporate the recommendations outlined above, the SSBCI will play an important role in supporting the recovery and resilience in the communities we serve.

Footnotes

- U.S. Department of Treasury. (2021). “ State Small Business Credit Initiative Preliminary Allocation Table”. https://home.treasury.gov/system/files/256/Preliminary-Allocation-for-States-Decline-in-Employment.pdf ↩︎

- Congressional Research Service. (2021). “State Small Business Credit Initiative: Implementation and Funding Issues”.https://fas.org/sgp/crs/misc/R42581.pdf ↩︎

- Michael Eggleston and Lisa Locke. (2018). “The State Small Business Credit Initiative”. Policy insight: Community Development at the St. Louis Federal Reserve. https://www.stlouisfed.org/~/media/Files/PDFs/Community-Development/Policy-Insights/SSBCI_Policy_Brief.pdf?la=en ↩︎

- Michael Eggleston and Lisa Locke. (2018). “The State Small Business Credit Initiative”. Policy insight: Community Development at the St. Louis Federal Reserve. https://www.stlouisfed.org/~/media/Files/PDFs/Community-Development/Policy-Insights/SSBCI_Policy_Brief.pdf?la=en ↩︎

- Michael Eggleston and Lisa Locke. (2018). “The State Small Business Credit Initiative”. Policy insight: Community Development at the St. Louis Federal Reserve. https://www.stlouisfed.org/~/media/Files/PDFs/Community-Development/Policy-Insights/SSBCI_Policy_Brief.pdf?la=en ↩︎