Homeownership is a key strategy for HOPE to help build wealth and strengthen communities in the Deep South. For most families who own a home, their home is their largest asset and also their largest expense.1 Those expenses are increasing. From rising costs for construction and renovations to increased mortgage financing costs from both higher interest rates and rising closing costs, buying a home is becoming less affordable. Additionally, the costs of maintaining homeownership are rising, potentially threatening future wealth gains.2

This blog specifically looks at homeowners insurance across this Deep South, considering both premium increases as well as policy availability, compared to the rest of the country. The data show that despite having lower incomes and lower property values, the Deep South has some of the highest homeowners insurance rates and some of the largest increases in premiums over the last several years.

An increase in homeowners insurance can lead to an increase in the monthly mortgage payment for homeowners, as these payments include the escrow payments for those insurance costs, along with the borrowers’ payments for principal, interest, and taxes. An increase in insurance premiums can then, in some cases, make their monthly payments unaffordable, especially for families that are already operating with little to no savings. Families may be forced to make tough decisions about the insurance coverage they can afford. Some families have been forced to settle for insurance coverage that requires them to take on more risk by choosing policies that provide less coverage or that require higher deductibles before coverage takes effect.

Insurance costs are a greater share of incomes and are rising in the Deep South while the assets protected decline in value

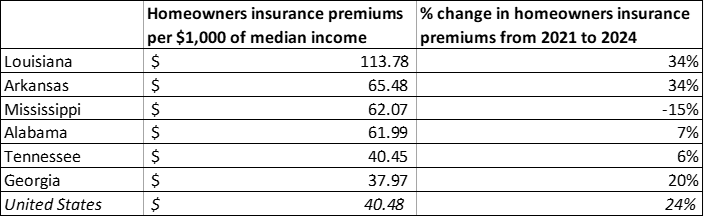

According to data from the Consumer Federation of America, from 2021 to 2024, annual insurance premiums for a typical homeowner increased by an average of $648, or 24%, across the country.3 Annual premiums were slightly larger in rural areas with $3,317 in 2024 than premiums for urban and suburban homes ($3,299).4 In Deep South states, rates in Arkansas and Louisiana increased by 34% from 2021 to 2024, and the city of New Orleans had the highest increase during that time period among metropolitan areas in the Deep South and the second highest nationally, with average rates increasing by 58% to over $10,000 annually.

Table 1 below shows the average homeowners insurance premium increases by state from 2021 to 2024 and what that looks like as a share of income, or the average premium per $1,000 of median income. The data show that some areas of the Deep South have experienced large increases in premiums, while others, like Mississippi, have fallen in recent years. However, despite some recent declines, when premiums are considered as a portion of income, the premium paid per $1,000 of income in Mississippi is more than $20 higher than the national average. Overall, someone earning the median income in Mississippi ($59,127) will pay more than $1,200 more per year in premiums than the national average. With overall lower incomes across the Deep South than elsewhere, families that are already income-strapped are paying a greater share of their income towards insurance premiums.

Table 1: Percent Change in Homeowners Insurance Premiums in Deep South, 2021-2024

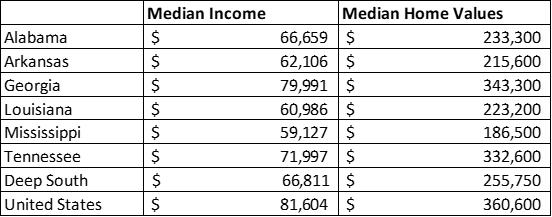

Three out of the four states with the lowest median household incomes nationally are located in the Deep South, including, Arkansas, Louisiana, and Mississippi. Mississippi is the only state with a median household income below $60,000. The median household income in Deep South states combined is $66,811, or $14,793 less than the national median income. The impact of increases in homeowners’ insurance premiums is magnified for families with lower incomes, especially with the current widespread increases in other essential household expenses like food, utilities, and gas as discussed in a recent HOPE blog on affordability.

In addition to lower income levels, home values in the Deep South also trail behind other regions. See Table 2. The median home value in the Deep South is $255,750 with some significantly lower, like Mississippi ($186,500). The Deep South median home value is about 30% lower than the national median home value of $360,600.5 When incomes, home values, and insurance premiums are looked at together, homeowners in the region are increasingly paying more to protect assets that relatively provide a smaller amount of wealth.

Table 2: Median Income and Median Home Values by State

Access and affordability of homeowners insurance is decreasing

In many cases, insurance providers increase premiums for certain homeowners partially based on the homeowners’ credit scores. Lower credit scores can lead to higher insurance premiums. While some states like California, Maryland, and Massachusetts do not allow insurance companies to base premiums on credit scores, people in the Deep South face large premium increases based on credit score with 100-149% increases in Arkansas, Georgia, Mississippi, and Tennessee and 50-99% increases in Alabama and Louisiana.6 Research shows that these increases have outpaced increases in insurance premiums due to disaster risk.7 Basing insurance premiums on credit scores skews rates higher for homeowners with lower incomes, rural residents, and people of color who have lower credit scores, ultimately making homeownership less affordable for those groups.8

For some homeowners, instead of increasing premiums, their insurance provider has dropped them altogether, and they must find a new insurance policy. This may require trade-offs of higher costs or lower coverage to find a new policy. Some states, including Alabama, Georgia, Louisiana, and Mississippi, have insurers of last resort for properties that cannot get insurance through private insurers. Reliance on these plans has increased in recent years with an almost 80% increase as a percent of market share from 2019 (1.4%) to 2023 (2.5%). Louisiana was among the top two states in the highest market share for state insurers of last resort with more than 5% market share.9

As a mortgage lender, HOPE recognizes the importance of homeownership to the stability and financial security of families. Homeownership offers financial stability and is the single largest pathway to building wealth for most families.10 It is a cornerstone of thriving neighborhoods, yet today, owning a home is increasingly out of reach for many households. Rising homeowners insurance costs are a growing threat to affordability, financial stability, and hard-won gains in homeownership, particularly in the Deep South where households on average have lower incomes. When insurance premiums grow faster than incomes, families are forced into difficult choices that increase financial risk, undermine long term wealth building, and, in some cases, jeopardize their ability to remain homeowners at all. Addressing the challenges of insurance affordability and availability is key to ensuring people in the Deep South continue to be able to build intergenerational wealth and strong communities through homeownership.

Footnotes

- US Census Data Survey of Income and Program Participation “Wealth and Asset Ownership 2023” July 2025 available at https://www.census.gov/data/tables/2023/demo/wealth/wealth-asset-ownership.html and Federal Reserve “Report on the Economic Well-Being of U.S. Households (SHED) in 2024” May 2025 available at https://www.federalreserve.gov/publications/2025-economic-well-being-of-us-households-in-2024-housing.htm ↩︎

- McCue, Daniel, Whitney Airgood-Obrycki and Peyton Whitney, “Rising Costs of Homeownership Are a Growing Burden” February 2025 available at https://www.jchs.harvard.edu/sites/default/files/research/files/harvard_jchs_homeowner_affordability_mccue_2025.pdf ↩︎

- Sharon Cornelissen, Douglas Heller, Ethan Weiland, and Michael DeLong, Consumer Federation of America, “Overburdened: The Dramatic Increase in Homeowners Insurance Premiums and its Impacts on American Homeowners” April 2025 available at https://consumerfed.org/wp-content/uploads/2025/03/OverburdenedReport.pdf ↩︎

- Id. ↩︎

- U.S. Census Bureau. “Selected Housing Characteristics.” American Community Survey, ACS 1-Year Estimates Data Profiles, Table DP04. ↩︎

- Birss, et al., Consumer Federation of America Climate & Community Institute “Penalized: The Hidden Cost of Credit Score in Homeowners Insurance Premiums” August 2025 https://consumerfed.org/wp-content/uploads/2025/08/Penalized-Final.pdf ↩︎

- Id. ↩︎

- CFPB, “Consumer Finances in the Rural Areas of the Southern Region.,” June 2023, available at https://files.consumerfinance.gov/f/documents/cfpb_or-data-point_consumer-finances-in-rural-south_2023-06.pdf and “Consumer Finances in Rural Appalachia” September 2022, available at https://files.consumerfinance.gov/f/documents/cfpb_consumer-finances-in-rural-appalachia_report_2022-09.pdf ↩︎

- U.S. Government Accountability Office, “Homeowners Insurance: Premiums Generally Tracked Inflation by Rose More in Disaster Prone Areas” February 27, 2026 available at https://www.gao.gov/assets/gao-26-107867.pdf ↩︎

- Aladangady, Aditya, Jesse Bricker, Andrew C. Chang, Sarena Goodman, Jacob Krimmel, Kevin B. Moore, Sarah Reber, Alice Henriques Volz, and Richard A. Windle (2023). Changes in U.S. Family Finances from 2019 to 2022: Evidence from the Survey of Consumer Finances. Washington: Board of Governors of the Federal Reserve System, October, https://www.federalreserve.gov/publications/october-2023-changes-in-us-family-finances-from-2019-to-2022.htm ↩︎