Increasing Family Wealth and College Enrollment

May 18th, 2012

Enrolling in college and receiving a college degree became increasingly necessary for moving up the economic ladder and reaching reliable employment and sufficient wages. A family’s income affects the likelihood a recent high school graduate will enroll in college. But what about a family’s household wealth or assets? Findings from the Pew Charitable Trusts indicate that increases in a family’s wealth during high school years, as measured by changes in the value of their home, raise a student’s likelihood of enrolling in college.

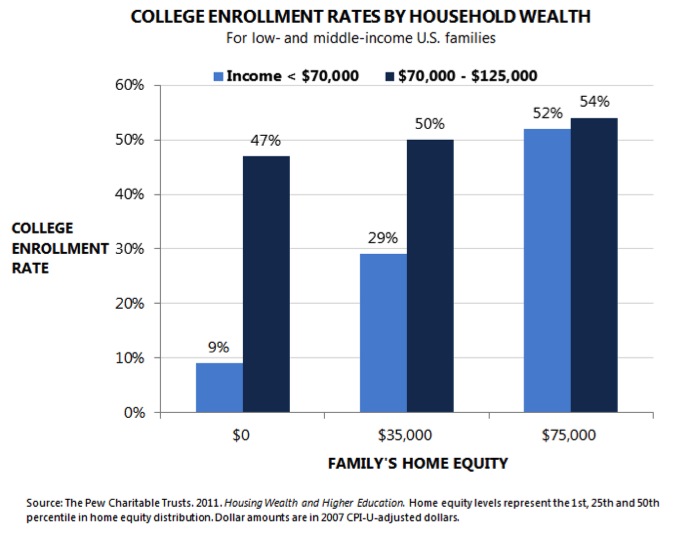

The chart shows college enrollment rates among students living in low- and middle-income families by the family’s home equity. For low-income families, having home equity at $35,000 (the 25th percentile) increased the college attendance rate from 9% to 29%. Enrollment rates rise to 52% when a low-income family’s home equity is $75,000 (50th percentile). Students from middle-income families also experience an increase in college enrollment as home equity rises.

Housing wealth could influence a student’s likelihood of enrolling in college for many reasons. The Pew report suggests that increases in housing wealth may affect college enrollment decisions because families use their wealth to directly finance education. Housing wealth could also indicate that a family has additional resources to set aside in a college savings account. It is also possible that families feel more economically secure, and open to helping their children navigate the path to applying for student loans to pay for a college education.

Low-wealth families may encounter more financial hurdles to supporting their children on the path to enrolling in post-secondary education. Efforts that promote wealth building among low and middle-income families and that support families in saving for a child’s education can lift more of Mississippi’s students to college enrollment and success.

Along with support for college savings, Community Development Financial Institutions (CDFIs) can connect underserved populations with a path to homeownership that builds wealth and home equity. Many CDFIs serve mortgage customers that are low- to moderate-income borrowers and first-time homeowners.

Supporting Mississippi’s families in accumulating college savings and broader wealth can lead to greater financial stability. Ultimately, these savings will result in an increased likelihood that more of Mississippi’s students pursue college courses and gain employment that allows them to save for their own families someday.

Read more on how home equity affects a student’s college decisions.

Author: Sarah Welker, Policy Analyst

Share this article.