State of Working Mississippi 2012 Chapter 4: PUBLIC INVESTMENTS, TAXES AND STATE REVENUE

February 8th, 2012

Chapter 4 of the MEPC’s State of Working Mississippi 2012 report examines the effect of taxes on Mississippi’s working families and makes some recommendations for reform.

Taxes are important to working Mississippians not just because they represent a portion of their paychecks, but also because they fund the public structures that provide the foundation for creating jobs and building a strong economy. Employers and workers alike need quality and accessible K-12 and higher education systems, strong infrastructure and safe communities. These structures require adequate resources. However state general fund revenues are estimated to still be down almost $250 million for FY 2013 from their peak in FY 2008.

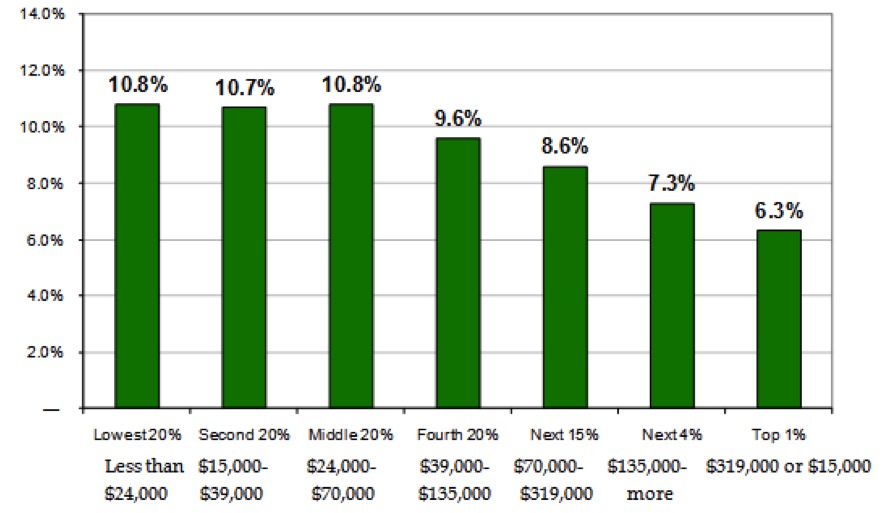

Taxes should be equitable and structured based on a worker’s ability to pay. While Mississippi’s tax system has both progressive and regressive elements (see definitions in Key Terms box), as a whole the state’s tax system is regressive. The table below shows that earners with lower incomes (less than $39,000 per year) pay over 10% of their income in state and local taxes, while those earning over $70,000 pay less. The top 1% of earners (those earning $319,000 or more annually) pay only 6.3% of their income in taxes.

ESTIMATED PERCENT OF INCOME PAID IN STATE & LOCAL TAXES BY INCOME QUINTILE IN 2007

The regressive tax structure exacerbates the state’s already significant income inequality. Income tax brackets have not been updated in more than 25 years. During that time, persons with higher incomes experienced substantial income gains compared with low-income residents.

In addition to reforms of the state’s tax structure, transparency is also necessary to make sure the public is getting the most out of economic development efforts, many of which are administered through the tax code.

RECOMMENDATIONS

- Update the income tax to create higher income tax brackets and make the tax more progressive. A new rate of 6% on taxable income over $45,000 (which is $64,600 of total earnings for a family of 4) and 7.5% on income over $100,000 would bring in an estimated $117 million through the personal income tax and $150 million through the corporate income tax.

- Broaden the sales tax to include more services. Including 21 new services in the sales tax as recommended by the Governor’s Tax Study Commission would bring in an estimated $98 million, and including all services used by households would bring in an estimated $287 million annually.

- Close corporate income tax loopholes. While there is no publicly available estimate of the amount of money lost to corporate tax loopholes, the measure would bring in additional revenue and make corporate taxes more fair for local businesses.

- Require more regular review of corporate tax credits and provide information to the public in order to determine whether the tax breaks really create jobs and help the economy.

Share this article.