FDIC and OCC Rent-A-Bank Proposals Put Deep South Families at Risk of Predatory Lending

January 16th, 2020

Two federal banking regulators are considering proposals that will encourage banks to partner with high-cost lenders to make loans that keep people trapped in a cycle of debt. The proposals will revive an approach seen before and historically known as rent-a-bank. This name stems from the nature of the partnership in which the lenders essentially “rent” the banks’ ability to make loans at unlimited interest rates, even when such rates exceed what is permitted under state law for nonbank lenders.

In response to the financial harm created by the rent-a-bank approach in the mid-1990s and early 2000s, federal regulators and states implemented commonsense reforms to protect consumers. As a result, this type of predatory lending was largely dormant – until recently.

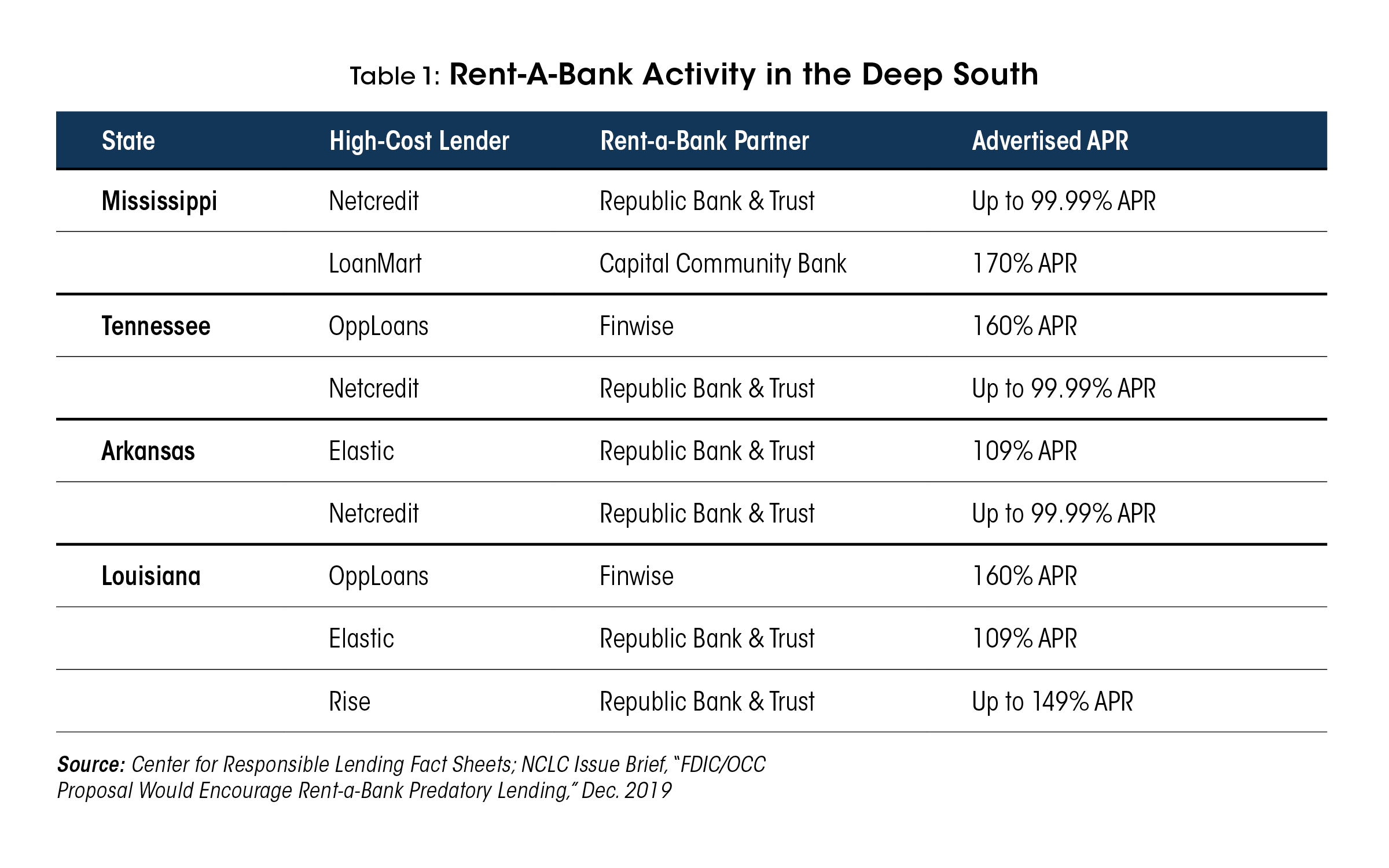

Predatory lenders and a few banks have revived the approach to exploit the financial situation of low-income borrowers. Unfortunately, this already includes nonbank lenders and out-of-region banks engaging in such activity here in the Deep South.[i] In Mississippi, Louisiana, Tennessee, and Arkansas, there is at least two lenders already implementing the approach to make high-cost loans online that would otherwise not be permitted under state law. (Table 1).

The loans made by these lenders can range in size from $2,000 to $5,000, with terms lasting a few months to several years. For example, a $3,000 Opploan in Tennessee carries a 160% APR, resulting in a total payback amount of $6,175 at the end of a year. A $2,000 Rise loan in Louisiana, with 42 bi-weekly payments, carries a 148% APR, resulting in a payback amount of $7,980.

The concerns about the FDIC and OCC’s proposals are not hypothetical. HOPE members and the communities in which HOPE branches are located have encountered predatory loans originated under the rent-a-bank approach. The high-cost loans create a debt trap that is nearly impossible to escape and push people into deeper financial trouble, including the increased likelihood of involuntary bank account closures.

These loans and their consequences are of particular concern in the Deep South, which already faces the highest rates of unbanked households in the country, along with high levels of credit insecurity. In each of these Deep South states, more than 30% or more of all households are unbanked or underbanked, which is higher than the national average (27%). The proposals will exacerbate these disparities.

The FDIC and OCC should take action to rein in the predatory nature of the rent-a-bank arrangements, rather than move forward with the proposals to expand it. Both agencies are accepting comments on their rent-a-bank proposals. Join us in urging the federal regulators to reject these proposals, which will expand predatory lending in our region.

Add your voice today by submitting a comment at the links below:

- OCC, Deadline: Jan. 22, https://www.regulations.gov/comment?D=OCC-2019-0027-0001

- FDIC, Deadline: Feb. 4, https://www.federalregister.gov/documents/2019/12/06/2019-25689/federal-interest-rate-authority

[i] Nonbank lender (location): Netcredit (Illinois); LoanMart (California); Opploans (Illinois); Elastic (Texas); Rise (Texas). Bank (location): Republic Bank and Trust (Kentucky); Finwise (Utah); Capital Community Bank (Utah)

Share this article.