Protecting Communities from the Rollback of CRA Reforms

August 19th, 2025

By Sara Miller, Senior Policy Analyst

The Community Reinvestment Act (CRA), enacted in 1977, was designed to combat the lasting impacts of redlining and ensure that banks meet the credit needs of all communities, including low-income neighborhoods and communities of color. For decades, CRA has been one of the few tools available to hold banks accountable for reinvesting in the places where they operate.

In 2023, after years of collaboration between regulators, banks, and community stakeholders, long-overdue updates to CRA were finalized – the first significant update to CRA since 1995. These reforms modernized the law to reflect today’s banking realities—including the rise of online and mobile banking and the decline of traditional bank branches. The new rules expanded banks’ assessment areas beyond physical locations, ensuring that rural communities, small towns, and underserved urban areas would not be left behind.

Federal regulators, however, recently announced plans to rescind these reforms, reverting back to the former CRA rules of 1995. This rollback would strip away key improvements and make it easier for banks to collect deposits from communities without reinvestment.

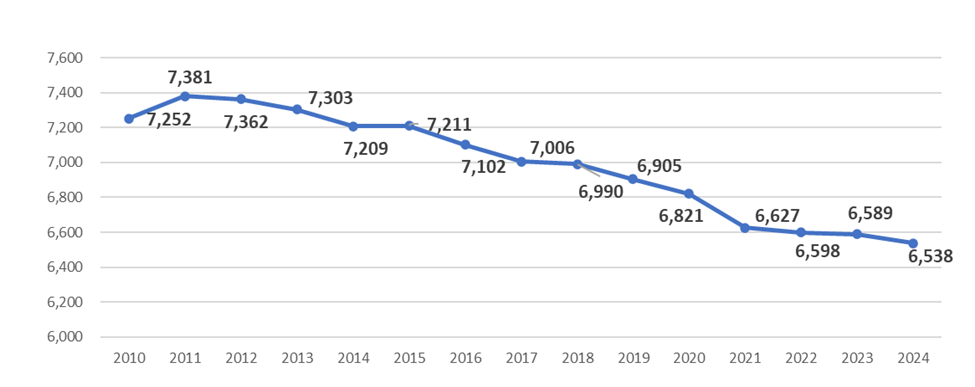

The stakes are high in the Deep South. This region already suffers from persistent poverty, widespread bank branch closures, and some of the highest rates of banking deserts in the country.[1] Since 2010, the Deep South has lost more than 800 branches—an 11% decline—with rural areas disproportionately affected (See Figure 1). Without modernized CRA standards, many of these communities will continue to be excluded from fair access to credit and investment. Banks will have no requirement to invest in areas in which they have no physical location.

Since 2010, the Deep South has lost more than 800 branches—an 11% decline—with rural areas disproportionately affected (See Figure 1). Without modernized CRA standards, many of these communities will continue to be excluded from fair access to credit and investment. Banks will have no requirement to invest in areas in which they have no physical location.

Figure 1: Number of Bank Branches in the Deep South 2010-2024

Source: Hope analysis of FDIC Historical Bank Data available at https://banks.data.fdic.gov/bankfind-suite/historical

Under the current (1995) rules, more than 95% of banks pass their CRA exams, despite the glaring inequities that persist in access to capital for underserved communities. Black and Hispanic residents make up the majority of those living in formerly redlined areas, which continue to face higher rates of vacancy, abandonment, and disinvestment. Passing grades do not reflect the current challenges of credit access and investment of communities historically affected by redlining.

Rolling back the 2023 reforms would represent a major setback for underserved communities across the nation. HOPE’s experience shows that CRA, when enforced effectively, can leverage significant resources to support equitable growth. Instead of retreating to past rules, regulators should build on the 2023 reforms to ensure that banks truly serve all communities—expanding access to credit, strengthening local economies, and addressing the enduring legacy of redlining.

[1] Hope Policy Institute. (2025). “CDFIs Provide Critical Financial Access Despite Growing Banking Desert, Report Finds”. http://hopepolicy.org/blog/cdfis-provide-critical-financial-access-despite-growing-banking-deserts-report-finds/

Share this article.