Breakout Session Wrap Up: Predatory Lending in Mississippi

November 4th, 2010

Payday loans have had a negative impact on working families and communities in Mississippi. During the 2010 Annual Policy Conference, a breakout session entitled “The High Cost of Being Poor: Lending Reform in Mississippi” focused on the types of borrowers most often using payday lending services and the effects those services have on the communities in which they operate.

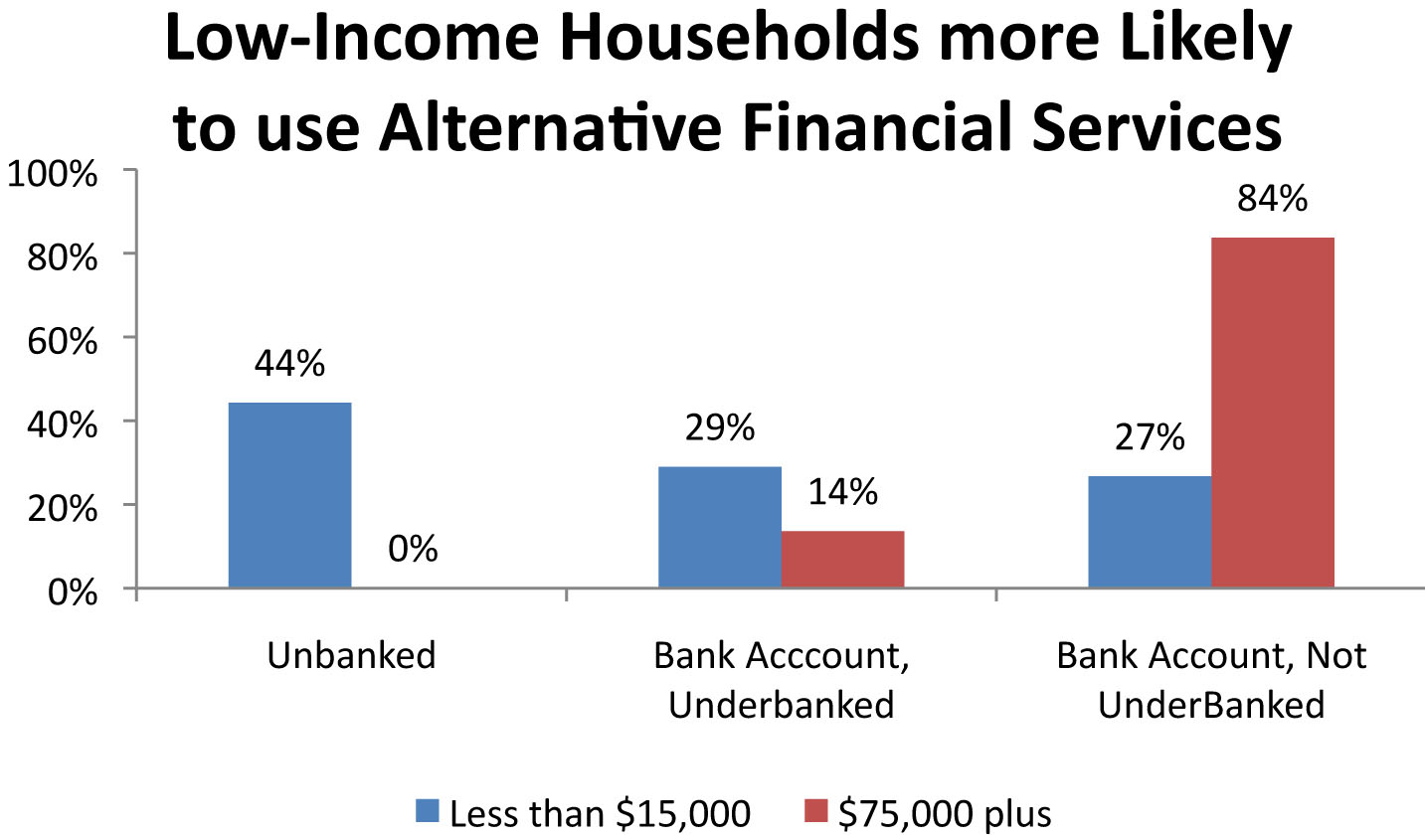

One of the concepts discussed was the high prevalence of Mississippi’s underbanked population with low-incomes. Underbanked means that an individual has a checking or savings account but relies on alternative financial services and has used non-bank money orders, non-bank check cashing services, payday loans, rent-to-own agreements, or pawnshops at least once or twice a year or refund anticipation loans at least once in the past five years. See Chart.

Click to enlarge

The finding helps explain one of the reasons why payday lenders tend to locate on main thoroughfares in or near economically distressed areas – access to potential customers. A number of local governments have expressed a desire to limit the number of check cashers due to the negative effects associated with high concentrations of those types of entities. The city of Ridgeland, for example, restricted the location of check cashers, title lenders and pawn shops due to their “blighting effect.” For more information on how to get involved with actions to reduce high-cost lending in Mississippi, readers can go to the website for the Mississippians for Fair Lending Coalition.

Source:

FDIC National Survey of Unbanked and Underbanked Households

Share this article.