CFPB’s New Report Highlights Unequal Banking Services and Debt Burdens for Consumers in the Rural South

July 19th, 2023

By Courtney Thomas, Senior Policy Analyst

The southern region is rich of social and cultural resources—characterized by a diverse population, strong community and familial bonds, lively cultural and art scene, and transformative social action. More than a third of the region are people of color, and over 70% of the United States’ rural black population calls the South their home.[1]

The CFPB recently released two new reports, Banking and Credit Access in the Southern Region of the US and Consumer Finances in the Rural Areas of the Southern Region that underscore the need for quality affordable financial services across the Deep South. These reports cover eight states, five of which are located in HOPE’s footprint, including Alabama, Arkansas, Louisiana, Mississippi, Georgia, North Carolina, South Carolina, and Tennessee. The reports highlight challenges and opportunities for growth in rural southern communities, particularly concerning bank account ownership, equitable access to credit, and consumer debt.

Access to Banking

The southern region has the highest unbanked rates in the country, the majority of which are in rural communities and communities of color.[2] In MS, the rural unbanked rate is twice as large as the unbanked rate of metro areas.[3] Furthermore, many areas in Mississippi are banking deserts. Nearly forty bank branches closed in the state between 2008 and 2018.[4]

HOPE’s five-state footprint of Alabama, Arkansas, Louisiana, Mississippi and Tennessee constitute the Deep South. Over nine million (6.2%) households are unbanked, which is nearly two points higher than the national percentage (4.5%).[5] Unbanked rates are starker among racial lines. In the Deep South, non-white households are six times more likely to be unbanked compared to white households.

While many households are unbanked, a vast majority are also underbanked. A household is considered underbanked when one or more individuals have a relationship with a financial institution, but the household still relies on alternative financial services such as payday loans or title loans to meet their financial needs. Similar racial disparities persist among underbanked households as unbanked households. Non-white households are two times more likely to be underbanked than white households.[6]

Table 1: Housing Characteristics by Banking Status of Deep South

Source: Hope Policy Analysis of 2021 FDIC Unbanked and Underbanked Data

Mortgage Loan Denial Rates

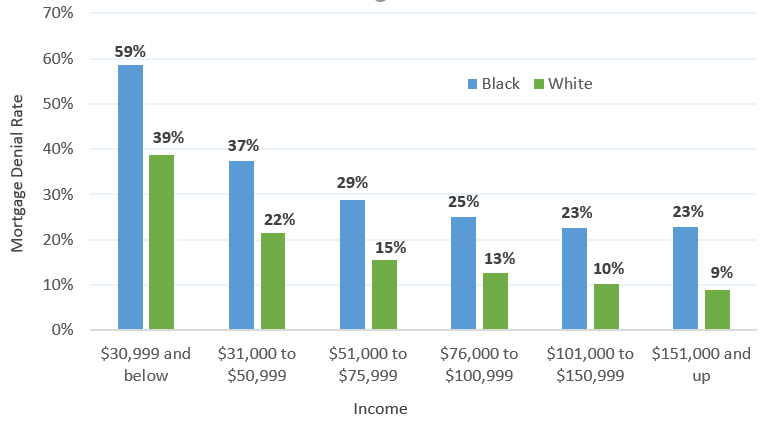

Homeownership continues to be a significant driver of wealth in the United States, and yet, there remains uneven access to this wealth-building tool. The CFPB report reveals that borrowers of color experience higher mortgage denial rates across all credit scores in both rural and non-rural communities.[7] There is consistently a lower share of loans to low- and -moderate-income borrowers and neighborhoods in rural counties than non-rural areas in the Southern region and nationally.[8] Within the Deep South, this phenomenon is also prevalent across income levels. For example, the denial rate for Black borrowers in the Deep South earning more than $150,000 was higher than for white borrowers earning between $30,000-$50,000.[9] See Figure 1. Consumers in rural persistent poverty counties in the South experience a 39% denial rate. [10]

Figure 1: Mortgage Denial Rates in the Deep South by Race and Income

Source: Hope Policy Institute Analysis of 2021 Home Mortgage Disclosure Act Data

Small Business Lending

Business ownership is key to closing the racial wealth gap. While White adults have thirteen times the wealth of Black adults, the gap closes to three to one when comparing the median wealth of white business owners to Black business owners.[11] The CFPB report illustrates several challenges that pose risks to business owners and their financial stability which affect the wealth gap. Establishing a banking relationship, access to credit for start-ups, collateral gaps, and increase of predatory lending were all cited as major barriers. HOPE analysis of its members corroborates the findings of the CFPB. Minority businesses in the Deep South continue to face capital shortfalls, and there is a strong need for collateral enhancements and initial injection capital. HOPE has observed an increase in minority business owners who turn to predatory lenders with seemingly “low-interest rates” but harsh repayment structures. This is evidenced by the borrower story below.

A local Memphis attorney and the founder of a property development company took out a merchant cash advance to acquire property for her business and do some capital improvements. The interest rate of the loan was 10%, but terms of the loan were extremely short– 6 months, and after the 6 months if they did not find a permanent loan, they would have to pay a fee to retain the short-term loan. The fee was $4,000 to extend the note for no more than 3 months. HOPE was able to refinance the investment property under very favorable terms. HOPE was able to reduce the rate by 3%. The new rate was 6.715% on a 15-year term, 25-year amortization for a 200 thousand dollar loan. The loan structure was subject to a rate adjustment every 5 years instead of every few months. With this loan, the borrower was able to restructure their balance sheet and able to retain additional cash flow for the business.

Consumer Debt

Debt is a major barrier to achieving financial sustainability. The CFPB report highlights the heavy debt burdens that Rural Southern consumers carry. Forty percent of rural southerners in majority-minority census tracts have subprime credit scores compared to 22% nationwide.[12] This makes them more susceptible to predatory lenders and high-interest-rate loans they cannot afford. Analysis from the Center for Responsible Lending report that payday and title loan lenders drained more than 400 million dollars in fees from consumers in the Deep South.[13] Auto loans and student loan debt present significant financial challenges for Southern borrowers. In the rural south, consumers are more dependent on vehicles for work and travel due to a lack of transit infrastructure. Furthermore, those who live in persistent poverty tracts have lower median incomes and higher debt-to-income ratios. Rural southerners in persistent poverty counties are twice as likely to be more delinquent on auto loans than consumers nationwide. Additionally, they are less likely to access income-driven student loan debt repayment plans.[14] All of this evidence suggests that rural southern communities will be impacted significantly as student loan debt forbearance and other state and federal relief efforts come to an end.

The CFPB reports confirm the lived experiences of Southern rural communities, especially Deep South households of color and persistent poverty areas. HOPE’s work closely aligns with the findings. More research is needed to expose the unique barriers and opportunities to increase financial stability for all families in the Deep South. Understanding the distinct challenges that southern rural communities face is key to creating a fair and equitable financial market that builds wealth for all.

[1] Consumer Financial Protection Bureau (2023). “ Banking and Credit Access in the Southern Region of the U.S. “ (2023) https://www.consumerfinance.gov/data-research/research-reports/banking-and-credit-access-in-the-southern-region-of-the-us/ [2] Federal Deposit Insurance Corporation. (2022). “2021 FDIC National Survey of Unbanked and Underbanked Households”. https://www.fdic.gov/analysis/household-survey/2021report.pdf [3] Consumer Financial Protection Bureau (2023). “ Banking and Credit Access in the Southern Region of the U.S. “ (2023) https://www.consumerfinance.gov/data-research/research-reports/banking-and-credit-access-in-the-southern-region-of-the-us/ [4] Ross, Janel (2019). NBC News, “A town with no bank: How Itta Bena, Mississippi, became a banking desert.” https://www.nbcnews.com/news/nbcblk/how-itta-bena-mississippi-became-banking-desert-n1017686 [5] Hope Policy Institute Analysis of 2021 FDIC National Survey of Unbanked and Underbanked Households.” [6] Ibid., [7] Consumer Financial Protection Bureau (2023). Banking and Credit Access in the Southern Region of the U.S. https://www.consumerfinance.gov/data-research/research-reports/banking-and-credit-access-in-the-southern-region-of-the-us/ [8] Ibid., [9] Hope Policy Institute analysis of 2021 Home Mortgage Disclosure Act data [10] Ibid., [11] Association for Enterprise Opportunity (2017). “Tapestry of Black Business Ownership in America: Untapped Opportunities for Success” [12] Consumer Financial Protection Bureau (2023). “ Consumer Finances in the Rural Areas of the Southern Region”

https://www.consumerfinance.gov/data-research/research-reports/consumer-finances-in-rural-areas-of-the-southern-region/

[13] Glottman, Sunny, Charla Rios, Lucina Constantine (2023). “The Debt Trap Drives the Fee Drain: Payday and Car-Title Lenders Drain Nearly $3 Billion in Fees Every Year.”https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-debt-trap-fee-drain-jun2023.pdf

[14] Consumer Financial Protection Bureau (2023). “ Consumer Finances in the Rural Areas of the Southern Region”https://www.consumerfinance.gov/data-research/research-reports/consumer-finances-in-rural-areas-of-the-southern-region/

Share this article.