Closing the Gap: Opportunities to Increase Secondary Mortgage Access for Rural Deep South Communities

March 16th, 2026

By Sara Miller and Diane Standaert

Secondary market investors currently have a tremendous opportunity to improve access to homeownership in rural Deep South communities. HOPE and other mission-based Community Development Finance Institutions (CDFIs) demonstrate that responsible, high-performing mortgage lending to borrowers with lower credit scores, no down payment, and nontraditional credit histories is not only possible, it is working. Through the secondary market, entities like Government Sponsored Enterprises (GSEs), banks, and other private investors can increase homeownership in rural areas in the Deep South by broadening the loans they purchase to include strong-performing loans such as these made by CDFIs. With reliable secondary market access, lenders like HOPE would be able to free up more funds to make more mortgage loans, serve more families, and increase access to homeownership for more people – demonstrating the policy and market-based solutions to increase access to the secondary market, as discussed here.

The Secondary Market Gap

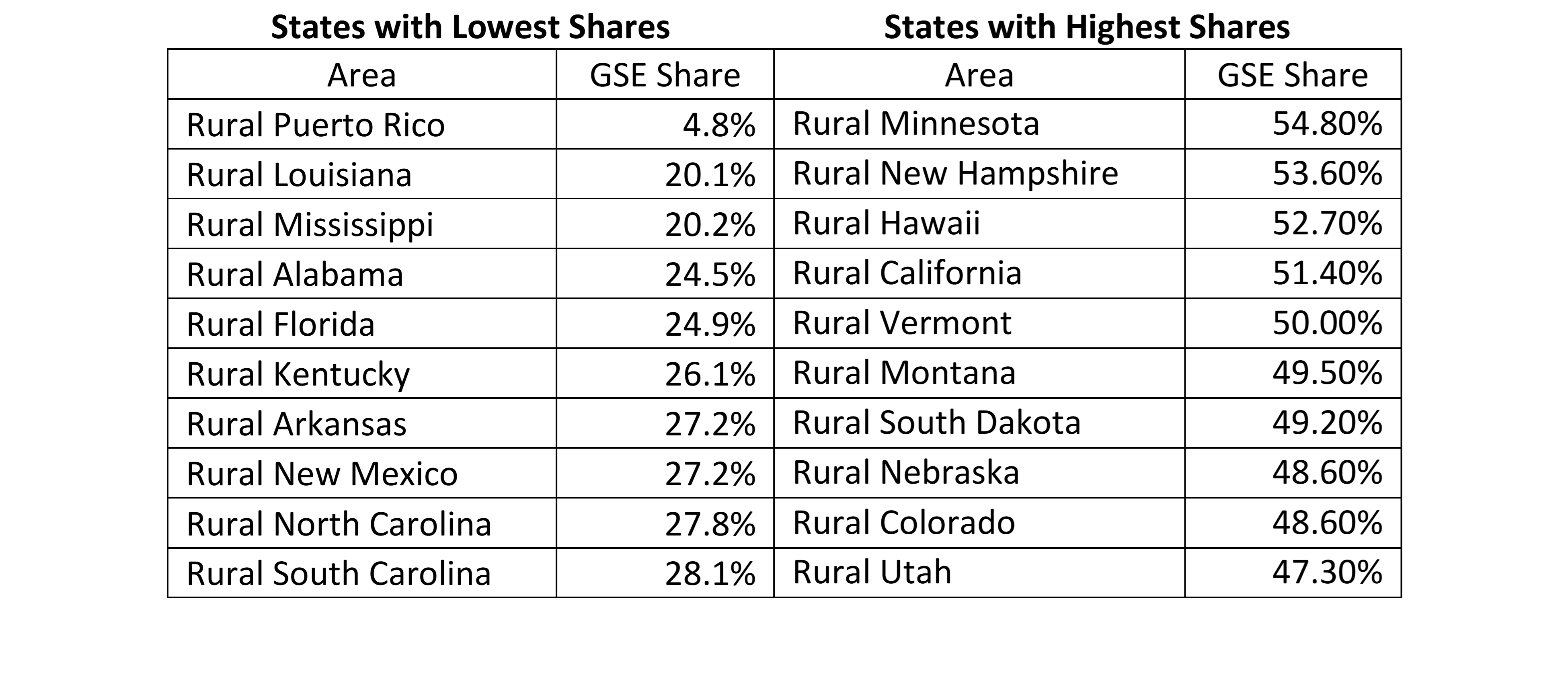

In 2024, only 1 in 5 mortgage loans in rural Mississippi or rural Louisiana were sold to Fannie or Freddie, according to a recent analysis from the Center for Mortgage Access. The report also shows how rural communities in the Deep South are not benefitting from Fannie and Freddie’s secondary market purchases as much as rural areas in other areas of the country. With shares of GSE loans ranging from 20 to 27%, rural LA, MS, AL, and AR are among the ten rural areas with the lowest share of GSE loans in rural markets across the country.[1] By comparison, in other rural areas like rural Minnesota and rural New Hampshire, the GSEs purchase more than 50% of mortgage loans. Table 1.

Table 1: Rural areas with the lowest and highest shares of single-family purchase and refinance loans purchased by the GSEs, 2024.

Source: Hope Policy Institute analysis of data from Center for Mortgage Access “Who Benefits from Government Mortgage Guarantees?” November 2025 available at https://mortgageaccesscenter.com/2025-11-04-Who-Benefits-From-Government-Mortgage-Guarantees/

Several factors contribute to the secondary market gap. Eligibility requirements for mortgage loans purchased on the secondary market often do not match the current economic realities of mortgage borrowers in Deep South underserved markets, like those identified by Fannie and Freddie as duty to serve communities in their Underserved Market Plans as high needs rural areas. As the largest purchasers of mortgages on the secondary market, Fannie Mae and Freddie Mac’s eligibility requirements have tremendous influence on the mortgages they will purchase and on the lending practices of the industry as a whole. Of note, Fannie Mae and Freddie Mac have taken some incremental steps to modernize their underwriting standards, including allowing positive rental payment history to be factored into credit assessments for borrowers with limited credit profiles.

The terms that define risk are another factor. The secondary market operates within a narrow “credit box” to determine loans eligible for purchase and uses a “risk-based” pricing structure that increases the costs to originate loans with characteristics that rural, Deep South borrowers in high needs rural areas are more likely to have, such as lower credit scores and higher loan-to-value ratios. Loans purchased by Fannie and Freddie in high needs rural areas under the Duty to Serve program had a 739 average credit score. Only 13% of those loans were to borrowers with a credit score lower than 680.[2] However, about 60% of consumers in rural persistent poverty counties in the South have a near-prime or lower credit status with a credit score under 660 – despite the fact that many potential homeowners have spent years successfully paying rent, utilities, and other obligations that never appear on a traditional credit report .[3] This gap reveals a mismatch between the GSE credit box and the economic realities of the families the Duty to Serve program was designed to reach.

As a result of these factors, HOPE and other CDFI lenders with similar products are effectively locked out of the secondary market. Consequently, they hold these loans on their balance sheets which limits their ability to increase loan volume given that no financial institution has unlimited balance sheet capacity. For instance, HOPE offers an in-house mortgage product, the Affordable Housing Program (AHP), designed to address several systemic obstacles for potential homebuyers from lacking a down payment to non-traditional credit history and other factors. These loans have performed very well with a low level of default and borrowers who have proven they can maintain homeownership when they are not priced out of the market with high costs products and fees.

HOPE’s Mortgage Lending

Through the AHP, mortgages are manually underwritten, and nontraditional indicators of credit repayment history are considered. Many potential homeowners have spent years successfully paying rent, utilities, and other obligations that never appear on a traditional credit report. The product also discounts deferred student debt, does not require mortgage insurance, and accepts credit scores as low as 580. The credit score is of significance. As the data shows above, borrowers in rural areas are much less likely to have the credit scores typically required from banks to qualify for affordable mortgages than their counterparts in urban areas.[4] Also, of critical importance, the AHP allows for a loan-to-value (LTV) of 100% – eliminating down payment barriers.

With the AHP product, HOPE’s mortgage portfolio has more than quadrupled from about $34 million in 2010 to $242 million in February 2026. Even with that growth, the scale of the need for accessible and affordable financing for housing and homeownership has not even come close to being exhausted. In 2025, HOPE provided mortgages to 497 borrowers, providing $94 million in capital, with 81% of loans to people of color, 60% to women, 87% to first-time homebuyers and 20% in non-metro areas. HOPE borrowers with mortgages made in 2025 had a median credit score of 668 and a median debt to income ratio of 40.8%. HOPE’s portfolio currently and historically has strong performance, with very low rates of default or loan loss. However, of the $94 million in mortgage loans originated by HOPE to serve 494 borrowers, just 71 of these loans ($18.5 million) were sold to the secondary market (GSEs, FHA, USDA loans). The vast majority of which were FHA loans, and only 17 ($2.9 million) were loans that were delivered to Fannie or Freddie.

Solutions to Close the Gap

There are several ways the secondary market can respond to these opportunities. First banks can do more to purchase mortgage loans such as these to help fill the access gap for lenders serving rural underserved markets. Not only are these successful loans for investment purposes, but they also, in some cases, could satisfy Community Reinvestment Act requirements. Second, GSEs can expand their eligibility requirements for loan purchases. This can be done through small pilot programs that would demonstrate the viability and impact of these purchases. One interim promising step is Fannie Mae’s recent amendment to its Underserved Market Plans for its Duty to Serve requirements is their intent to make deposits in Rural CDFIs, ultimately making more funds available for mortgage lending.

Finally, an innovative bipartisan proposal sponsored by thirty Senate co-sponsors called the Scaling Community Lenders Act and announced as part of the Access to Fair Financing for Opportunity and Resilient Development (AFFORD) Act, would allow U.S. Treasury’s Community Development Finance Institution Fund to support CDFIs through secondary market purchasing as well, providing long term liquidity that would allow CDFIs to scale up the impact of their mortgage lending as they can use the proceeds of each sale to fund another mortgage.

Creating a viable secondary market pathway for AHP-type loans would unlock a cycle of lending and reinvestment that could transform homeownership rates across the rural Deep South, not just for the families HOPE serves and the communities they live in today, but for generations to come.

[1] Scott Susin Center for Mortgage Access “Who Benefits from Government Mortgage Guarantees?” November 2025 available at https://mortgageaccesscenter.com/2025-11-04-Who-Benefits-From-Government-Mortgage-Guarantees/

[2] FHFA Duty to Serve 2024 Single Family Dashboard accessed February 2026 available at https://www.fhfa.gov/data/dashboard/dts/single-family/2024

[3] CFPB, “Consumer Finances in the Rural Areas of the Southern Region.,” June 2023, available at https://files.consumerfinance.gov/f/documents/cfpb_or-data-point_consumer-finances-in-rural-south_2023-06.pdf

[4] CFPB, “Consumer Finances in the Rural Areas of the Southern Region.,” June 2023, available at https://files.consumerfinance.gov/f/documents/cfpb_or-data-point_consumer-finances-in-rural-south_2023-06.pdf and “Consumer Finances in Rural Appalachia” September 2022, available at https://files.consumerfinance.gov/f/documents/cfpb_consumer-finances-in-rural-appalachia_report_2022-09.pdf

Share this article.