Combined Reporting Would Address Corporate Income Tax Loopholes and Level the Playing Field for Local Businesses

July 8th, 2011

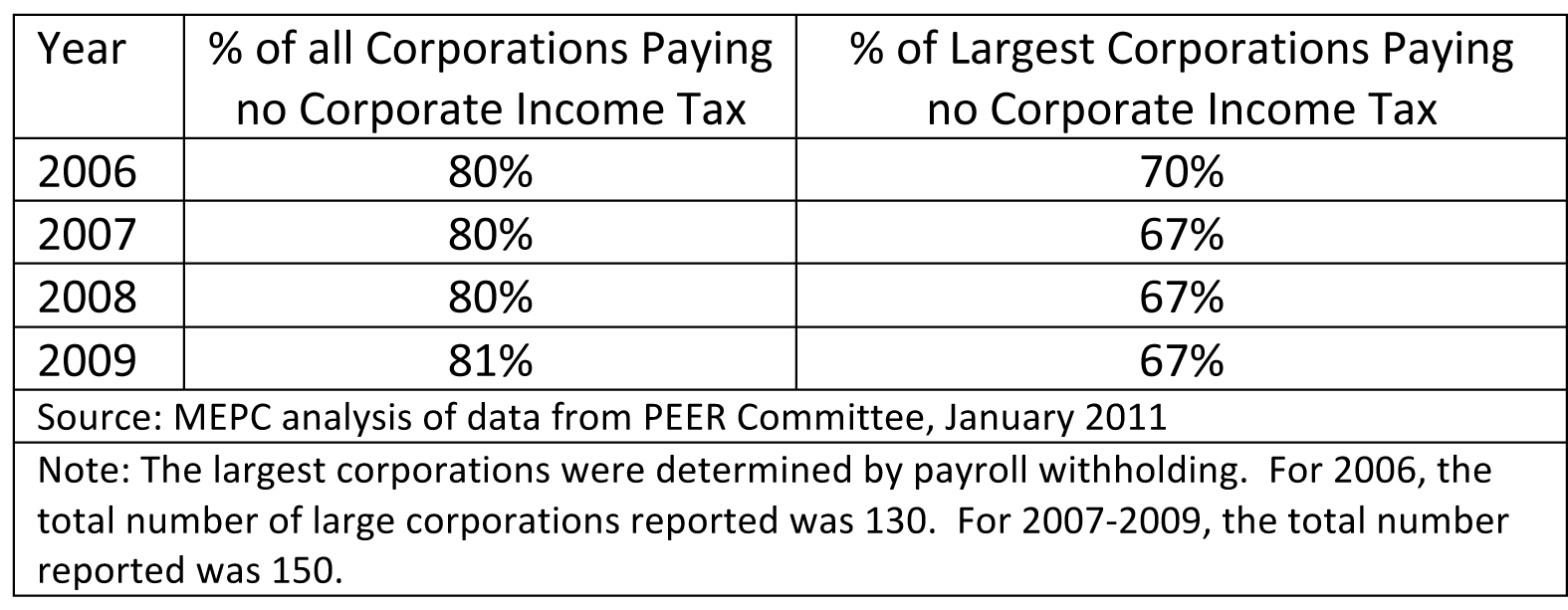

A news report this week brought new attention to research released earlier this year from the PEER Committee on corporate participation in the state’s corporate income tax. The research shows that approximately 80 percent of all corporations operating in Mississippi do not pay the state’s corporate income tax. The PEER data also shows that 70 percent of the largest corporations (as measured by payroll withholding) do not pay corporate income taxes. The PEER Committee examined tax data from 2006-2009. The large number of corporations paying no corporate income tax is striking, especially in the years of prosperity before the recession that affected corporate profits.

Click to enlarge

Corporations Operating in Mississippi Paying Zero State Income Tax 2006-2009

Corporate profits are subject to Mississippi state income taxes at the same rates and brackets as individual income taxes. The rates are 3 percent on the first $5,000, 4 percent on the next $5,000, and 5 percent on profits over $10,000. Possible reasons for not paying corporate income taxes include operating at a loss or shifting profits to related corporations in other states. One way to end the practice of shifting Mississippi profits to other states would be to require related multi-state corporations to report their income together – a practice known as combined reporting.

Most large corporations that span multiple states are made up of parent corporations and a number of subsidiaries. Without combined reporting, such a corporation may be able to only file income taxes for one subsidiary in the state, which has transferred much of its income to the parent, or other subsidiaries to avoid taxation. Combined reporting requires such a company to report all of their income together from all subsidiaries in all states. Then, the share of income attributable to a company’s activity in the state is calculated, and the state’s corporate income tax rate is applied.

Combined reporting is not a tax raising measure. It is a measure that disallows tax avoidance methods that are not available to all taxpayers. Small businesses operating in Mississippi, for the most part, do not have the means to take advantage of transferring income out of state to avoid taxation. Combined reporting would level the playing field for the large multi-state corporations and local small businesses.

Share this article.