Federal Agencies Propose Rules to Eliminate Excessive Junk Fees and Provide Crucial Protections for Vulnerable Consumers

March 29th, 2024

By Courtney Thomas, Senior Policy Analyst

In a trifecta win for consumers, the Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC) announced three highly anticipated proposed rules that will eliminate billions of dollars in excessive overdraft fees, non-sufficient fund (NSF) fees, and automobile fees. These rules, collectively, increase regulation of junk fees—-hidden or excessive fees that consumers pay for duplicative or unwanted services. Junk fees disproportionately affect communities of color and cash-strapped families. The CFPB estimates that junk fees cost consumers nearly $29 billion every year.[1] The proposed rules will provide meaningful safeguards for consumers and are expected to return at least $7 billion to consumers annually.[2]

Overdraft Fees

Under the proposed overdraft rule, financial institutions with assets of $10 billion or more will be required to comply with updated Truth in Lending Act (TILA) regulations if they choose to offer overdraft products. They will have two options. Under the first option, banks and credit unions can still charge an overdraft fee, but the fee can only cover the amount that a financial institution needs to “break-even” or otherwise recuperate their loss. The CFPB has proposed benchmarks of $3, $6, $7, or $14 for overdraft fees or banks can set an overdraft fee as determined by their costs to breakeven. Under the second option, banks can provide an overdraft loan but will have to comply with long-standing truth in lending laws by offering clear disclosures and consumer protections.

The rule currently only applies to very large financial institutions, roughly 175 banks, and 22 credit unions, which the CFPB estimates are responsible for over two-thirds of the total market-wide overdraft fee revenue. It is likely to expand to cover smaller institutions thereby providing greater consumer protections across the banking industry.

Non-Sufficient Funds Fees

The CFPB also announced a proposed rule on NSF fees that will prohibit non-sufficient fund fees on debit card transactions and peer-to-peer payments that are declined instantaneously. The CFPB is aware that there are very few instances where financial institutions charge an NSF fees for these types of transactions. Most banks and credit unions levy NSF fees only on returned checks or ACH payments. Nonetheless, this rule sets an important position on reforming the practice of junk fees within the financial industry and prevents corporations from what Director Chopra describes as, “concocting new fees for services that cost little to nothing to deliver.”[3]

Overall, overdraft and NSF fees disproportionately impact financially vulnerable consumers. Consumers who have higher rates of overdraft transactions and NSF fees tend to have lower incomes, lower credit scores, and lower median deposits than non-overdrafters.[4] In particular, Black and Hispanic account holders are 1.9 times and 1.4 times more likely to overdraft their accounts than white account holders, respectively.[5] Multiple overdrafts and unpaid fees can also force financial institutions to close a person’s bank account and report the customer to the credit reporting agency –all of which make it more difficult for a consumer to open an account in the future. Excessive overdraft fees can create another financial burden and lead to widespread distrust among banking institutions for working families also. Distrust is among the leading reasons individuals do not have bank accounts.[6]

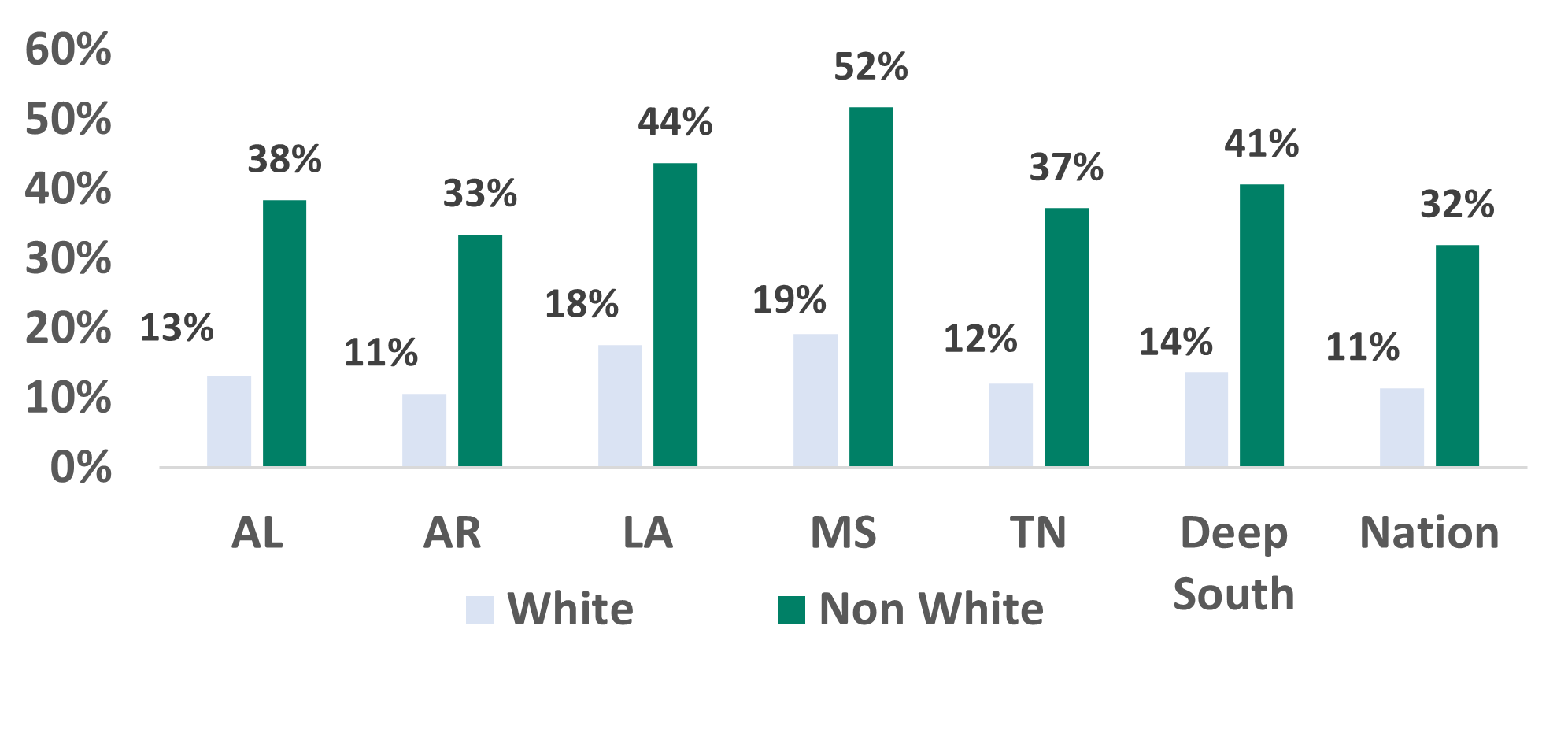

Households with no bank accounts are highly concentrated in the Deep South. In fact, the Deep South has the highest unbanked and underbanked rates in the country. Nearly 9% of households are unbanked, 14% are households of color.[v7] Households in Mississippi are almost twice as likely (11%) to be unbanked than the average American family (6%).[8] The unbanked rate doubles for households in rural communities compared to metros.[9] See Figure 1. This can be attributed in part to high poverty rates and distrust among financial institutions. The FDIC finds that the inability to meet minimum account requirements and distrust of banks as the top two reasons why they did not have a bank account. In the Deep South, limiting overdraft and NSF fees can improve confidence in the banking system in a region that has higher rates of unbanked and underbanked households.

Figure 1: Unbanked and Underbanked Rates in Deep South by Race

Source: Hope Policy Institute Analysis of 2021 FDIC Data[10]

Auto Retail Fees

The FTC announced the Combatting Auto Retail Scams CARs rule, which will eliminate “bait and switch” tactics that misrepresent financing and hide add-on fees in contracts which can have racial implications .[11] The FTC is actively enforcing regulations to decrease junk fees and abusive schemes, in addition to this proposed rule. For example, in 2022, the FTC took action against Passport Automotive Group for Illegally charging junk fees and discriminating against Black and Latino Customers. [12] The group was accused of creating fake mailers to lure consumers to dealerships and misrepresenting the price of their vehicles. Additionally, Black and Latino borrowers were charged more in financing costs than their white counterparts. The company will pay $3.3 million to harmed consumers.

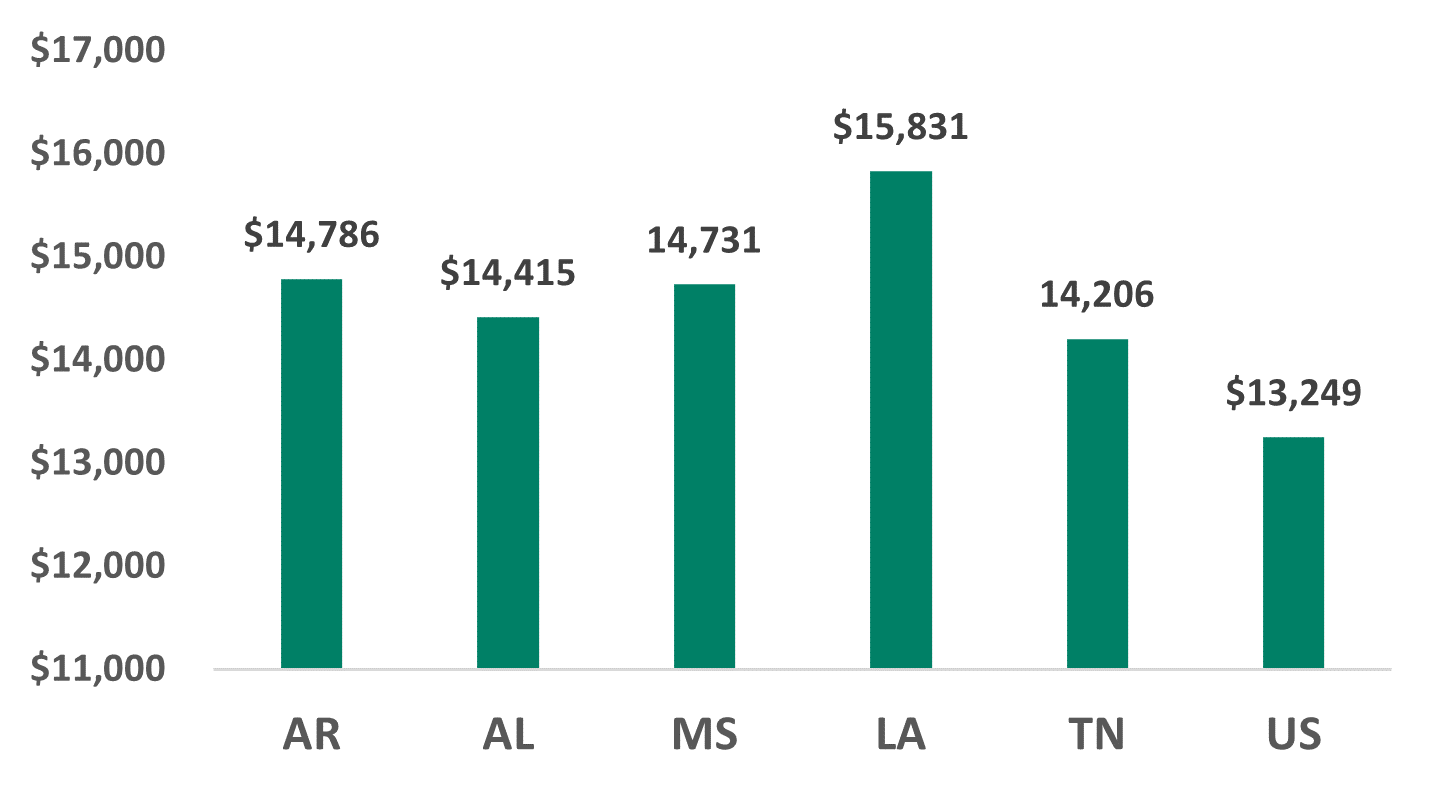

The CARs rule is likely to have positive effects on rural Deep South households who rely heavily on vehicles to commute to work and move freely around their neighborhoods. The rule is particularly significant given that Deep South consumers have higher auto loan balances and any savings and protections against abuse will better secure consumers access to transportation. The median balance outstanding on auto loans in the rural south is higher compared to the national average.[13] See Figure 2.

Figure 2: Median Auto Loan Balances in Deep South

Source: Hope Policy Institute Analysis of CFPB Median Auto Loan Balance[14]

Furthermore, wages are considerably lower in the South compared to the rest of the country, so it can be assumed that Southern consumers face higher auto debt burdens than their counterparts. The CFPB reports that in southern rural persistent poverty counties (PPCs), the median auto loan balance is nearly half of the median household income.[15]

These proposed rules are a long-awaited opportunity to increase consumer protections for financially vulnerable consumers. A fair and equitable financial system does not extract wealth from those most in need. We must continue to fight for policies that protect consumers and increase economic mobility for all.

[1] Pichee, Aimee. (2022).“Americans pay billions of dollars in junk fees every year. Here are some of the worst”. https://www.cbsnews.com/news/junk-fees-overdraft-fees-banks-cfpb/

[2]The $7 billion estimate reflects the sum of the FTC and CFPB estimated consumer savings from each proposed rule. Federal Trade Commission. (2024). “ FTC Pauses CARS Rule Effective Date. (2024, January 18)”.. https://www.ftc.gov/news-events/news/press-releases/2024/01/ftc-pauses-cars-rule-effective-date; Consumer Financial Protection Bureau. (2024).”CFPB Proposes Rule to Close Bank Overdraft Loophole that Costs Americans Billions Each Year in Junk Fees”. https://www.consumerfinance.gov/about-us/newsroom/cfpb-proposes-rule-to-close-bank-overdraft-loophole-that-costs-americans-billions-each-year-in-junk-fees/

[3] Consumer Financial Protection Bureau. (2024). “CFPB Proposes Rule to Stop New Junk Fees on Bank Accounts”. https://www.consumerfinance.gov/about-us/newsroom/cfpb-proposes-rule-to-stop-new-junk-fees-on-bank-accounts/

[4] Thomas, Courtney. (2022). “Forthcoming Legislation Targets Predatory Overdraft and NSF Fees”. Hope Policy Institute. http://hopepolicy.org/blog/forthcoming-legislation-targets-predatory-overdraft-and-nsf-fees/

[5] Smith, P., Babar, S., & Borne, R. (2020). “Overdraft Fees: Banks Must Stop Gouging Consumers During the Covid-19 Crisis”. Center for Responsible Lending. https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-overdraft-covid19-jun2019.pdf

[6] Federal Deposit Insurance Corporation.(2022). “2021 FDIC National Survey of Unbanked and Underbanked Households”. https://www.fdic.gov/analysis/household-survey/2021report.pdf

[7] Ibid.

[8] Ibid.,

[9] Consumer Financial Protection Bureau (2023). “ Consumer Finances in the Rural Areas of the Southern Region”

[10] Hope Policy Institute Analysis of FDIC (2021) National Survey of Unbanked and Underbanked Households. https://www.fdic.gov/analysis/household-survey/index.html

[11] The Federal Trade Commission. (2023).“FTC Announces CARS Rule to Fight Scams in Vehicle Shopping.”

[12] Federal Trade Commission . (2022). “Federal Trade Commission Takes Action Against Passport Automotive Group for Illegally Charging Junk Fees and Discriminating Against Black and Latino Customers”..

[13] Consumer Financial Protection Bureau.(2023). “Consumer Finances in the Rural Areas of the Southern Region”

[14] Ibid.

[15] Ibid.

Share this article.