Federal Consumer Protections Must Act as Buoy for Rural Borrowers Drowning in Debt

July 27th, 2021

Calandra Davis, Senior Policy Analyst

Christina Washington, Policy Intern

Even before the pandemic, people living in the Deep South were drowning in debt simply trying to meet basic needs. Now, a year and a half into the pandemic, harmful debt practices continue to hinder the economic security and mobility of rural households in the Deep South. Rural communities are plagued with the interconnectedness of low-incomes, extractive practices, and oppressive debt that reinforce cycles of inequity. Policy makers must account for the pervasive racial and economic inequality, and must prioritize protection from debt-related abuses. Consumer protections not only curb predatory lending and harmful debt practices that inhibit economic mobility, they also keep money in people’s pockets. Solutions such as: preventing predatory lending through a 36% rate cap, easing existing burdens of criminal justice debt or medical debt, and cancelling student loan debt remain critical for positioning people to move beyond the economic crisis that has been exacerbated by the pandemic.

Payday and Car Title Lending

In Deep South states, high-cost lenders saturate communities. Fees drained annually by payday and car title lenders total more than $1.6 billion in the four states of Alabama, Louisiana, Mississippi and Tennessee – among the ten highest in the nation.[1] The devastating financial consequences of high cost, predatory loans would be troubling for anyone, but they are particularly pronounced in rural communities, where economic inequality is deeply entrenched, and persistent poverty is prevalent. Communities of color, particularly Black and rural communities, experience higher rates of unbanked and underbanked households, making them easy targets for payday lenders who advertise “accessible credit.” For example, in Coahoma County, a rural Mississippi county with a Black population of 80%, the unbanked rate for households is 19%; triple the national rate.[2] Coahoma County has a per capita rate of 5 payday store fronts for every 10,000 people. In contrast, Desoto County, with a smaller Black population of 30%, has only 2 payday stores per capita.

Criminal Justice Debt

Criminal justice debt adds to the rising tide of debt in rural communities. Beyond the over saturation of payday lenders, Alabama, Louisiana, Mississippi, and Tennessee, are among the top 10 states with the highest incarceration rates in the country. In 2019, people in the Deep South were burdened by more than $4 billion in debt related to their interaction with the federal criminal system, more than double the amount from 10 years ago.[3] These debts are used to revoke state driver’s licenses, re-incarcerate people, prevent people from voting, and create significant barriers to achieving financial security.[4] Research by Alabama Appleseed shows that criminal justice debt feeds payday lending: A 2018 survey of almost 1,000 Alabamians who owed criminal justice debt showed that 44% of them took out payday or other high-cost loans to service it.[5]

Student Loan Debt

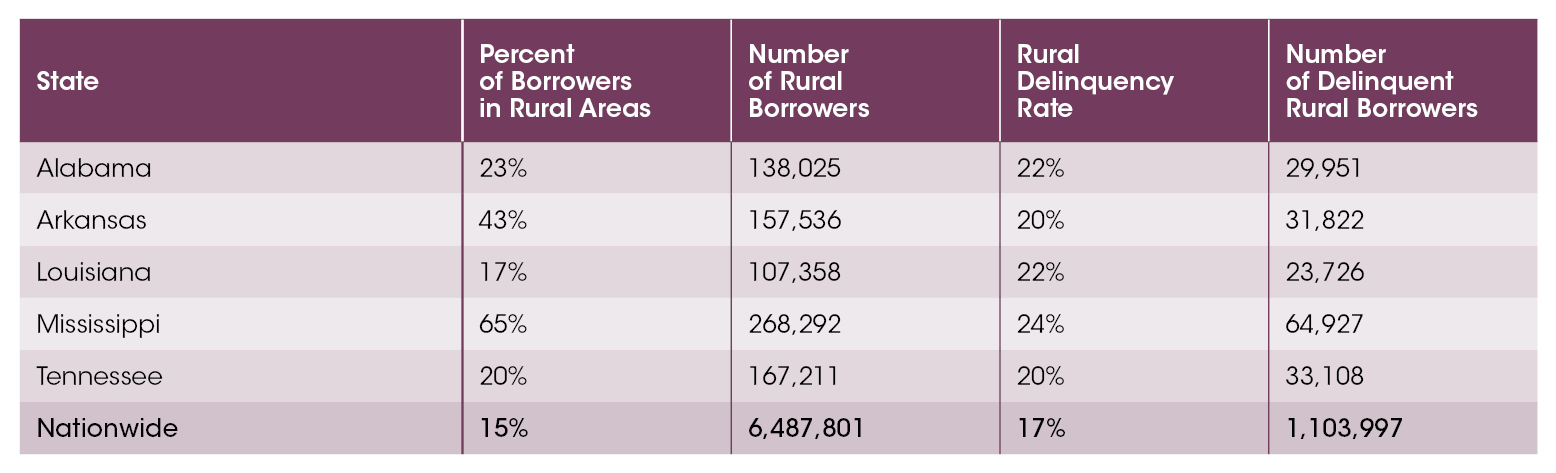

As rural borrowers wade through the sea of payday lenders, student loan and medical debt also loom large. Recent estimates indicate 6.5 million people in rural areas across the country each owe an average of $35,000 in student loan debt, and as many as 1.1 million rural student loan borrowers (nearly one-in-six rural borrowers) have fallen into delinquency or default (compared to roughly one-in-seven student loan borrowers nationwide). Borrowers who remain in rural areas after graduation also struggle more than their peers who migrate to metropolitan areas in other aspects of their financial lives. Deep South rural communities now have higher rates of student loan delinquency than rural communities elsewhere. Nationally, 17% of rural student loan borrowers are delinquent, but for each of the five Deep South states it is 20% or higher.[6] See Table 1.

Table 1: Student Debt Delinquencies in the Rural South

Source: Student Borrower Protection Center, Student Debt Crisis for Rural Borrowers. https://protectborrowers.org/wp-content/uploads/2020/12/Rural-student-debt-statistics.pdf

Furthering widening the gap is racial disparities in the collection of this student loan debt. In fact, the widest gap in the country exists in rural Monroe County, MS, where 45% of people with student loan debt in communities of color have this debt in collection, compared with 12% of people of student loan debt in white communities.[7]

Medical Debt

Nationally, medical debt and related collection abuses disproportionately harm rural and majority people of color communities, and stifle economic opportunity. This is of particular concern for Delta towns, where a history of discrimination and exclusionary policies, have led to high levels of economic distress, thus exacerbating both the burden and consequences of unaffordable debt. These conditions underscore the importance of policy solutions that provide debt relief. According to data by the Urban Institute, in Bolivar County, MS, one in four people in communities of color have a medical debt in collection, while white communities have a significantly lower rate.[8] Similar patterns are found across the Delta. Unless adequately addressed through debt collection protections or debt relief, medical debt will continue to deepen existing disparities in places like the Mississippi Delta and limit economic opportunity for local people and communities.

These debt mechanisms continue to be a barrier to financial mobility for rural households. Without federal protections, people impacted by the criminal system, stuck in student loan debt, burdened by medical debt, or harmed by predatory lenders lose out on wealth-building opportunities, deepening the cycle of inequities. As such, protections like a 36% rate cap for high-cost loans, student loan debt forgiveness, discharging and reducing criminal justice debt, and protecting against abusive debt collection practices are a necessary part of the equation for the economic recovery of the Deep South.

[1] Center for Responsible Lending, “Payday and Car-Title Lenders Drain Nearly $8 Billion in Fees Every Year,” April 2019, https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-statebystatefee-drain-apr2019.pdf

[2] Hope Policy Institute Analysis of July 2021 Prosperity Now Scorecard. https://scorecard.prosperitynow.org/data-by-location#county/28027

[3] United States Attorneys’ Annual Statistical Report. 2019. https://www.justice.gov/usao/page/file/1285951/download

[4] Calandra Davis, “Examining the Intersection Between Criminal Justice and Financial Services in the Deep South,” Hope Policy Institute, Jan. 13, 2021, http://hopepolicy.org/manage/wp-content/uploads/Criminal-JusticePaper.pdf.

[5] Alabama Appleseed, “Under Pressure: How fines and fees hurt people, undermine public safety, and drive Alabama’s racial wealth divide,” Oct. 2018, https://www.alabamaappleseed.org/wp-content/uploads/2018/10/AA1240-FinesandFees-10-10-FINAL.pdf

[6] Ben Kaufman and Vanessa Garcia Polanco, “Research Roundup: Rural Communities and Farmers are at the Forefront of the Student Debt Crisis,” Student Borrower Protection Center, Dec. 2, 2020, https://protectborrowers.org/research-roundup-rural-communities-and-farmers-are-at-the-forefront-of-thestudent-debt-crisis/.

[7] Hope Policy Institute of Analysis of The Student Debt Crisis for Rural Borrowers. https://protectborrowers.org/wp-content/uploads/2020/12/Rural-student-debt-statistics.pdf

[8] Hope Policy Institute Analysis of December 2020 from the U.S. Census Bureau and Urban Institute “Debt in America; An Interactive Dashboard”

Share this article.