Homeowner Assistance Funds critical to preserve Black homeownership throughout the Deep South

June 29th, 2021

As the nation seeks to recover from COVID-19, Deep South communities, especially communities of color, are precariously situated on the brink of economic and social devastation. Policy decisions made today have the opportunity to break, rather than repeat this cycle of inequity. Key among these decisions will be the protections afforded to people struggling to hold on to their homes, particularly borrowers of color and low-income borrowers who are among the hardest hit by COVID-19’s health and economic impacts. These same borrowers have also been most likely bypassed for other types of pandemic relief.

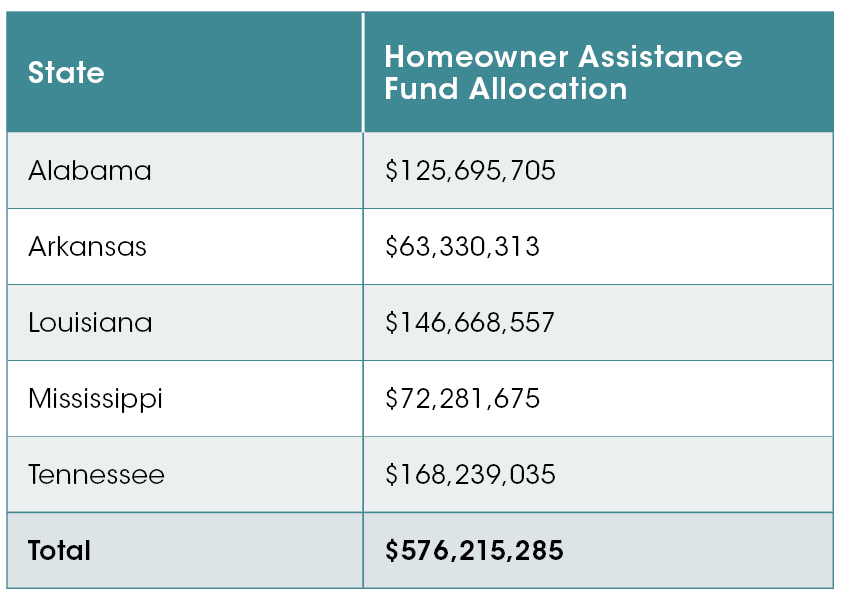

The Homeowner Assistance Fund, established by the American Rescue Plan and overseen by the U.S. Treasury, will provide funds to each state to help homeowners financially impacted by COVID-19 stay in their homes. Whether or not these funds reach homeowners most in need will depend on program design and community engagement. The opportunity is significant, as the Deep South is set to receive over half a billion dollars through the Homeowner Assistance Fund. See Table 1.

Table 1: Homeowner Assistance Fund Allocation in Deep South States

Source: U.S. Department of Treasury, “Homeowner Assistance Fund Data and Methodology for State and Territory Allocations,” April 14, 2021 available at https://home.treasury.gov/system/files/136/HAF-state-territory-data-and-allocations.pdf

This assistance and recommendations made here are offered against the backdrop of significant economic hardship for communities of color in the Deep South, which were more financially vulnerable prior to the pandemic due to a long history of discriminatory and exclusionary policies limiting people’s economic security. For example, in the late summer of 2020, in each Deep South state, over 50% of Black households had experienced a loss of employment income.[1] For Latino households, 70% in Arkansas and nearly 90% in Mississippi had experienced such a loss since the start of the pandemic. As of the end of 2020, Mississippi, Tennessee, and Louisiana had a nearly 12% Black unemployment rate, three times the white unemployment rate in those states.[2]

Recommendations for Equitable Deployment of Homeowner Assistance Funds

Community Engagement

Before programs are implemented, each state must submit a plan to the US Treasury department for review. One of the review criteria for the programs is the extent of each state program’s community engagement and public participation.[3]

To increase community engagement, program administrators should incorporate community input during the program design and implementation. Local organizations and community members that already provide assistance and support to homeowners have deep expertise and will contribute to the successful distribution of the funds.

Program administrators should convene a regular working group of stakeholders, including lenders and housing advocates, to walk through the program to troubleshoot in real time and to ensure the effective, efficient and equitable distribution of the available funds.

Ensuring Access for Underserved Homeowners

Program administrators should ensure homeowners most in need of assistance can access Homeowner Assistance Funds before the funds are fully deployed. To accomplish this goal, dedicated set asides should be created for socially and economically disadvantaged homeowners. First-come, first serve approaches to relief distribution reinforce inequities. Often people most in need more time or assistance developing and submitting applications for funds. The Small Business Administration Paycheck Protection Program reinforced this lesson. In addition, set-asides should run the duration of the program. Such an approach reaches more people in need than approaches that prioritize funding access for a short time at the beginning of the program launch.

Homeownership Assistance programs should also engage Community Development Financial Institutions to reach homeowners in persistent poverty counties. More than one-third of the nations’ persistent poverty counties are located in the Deep South. These counties are predominately rural and where a majority of the residents are people of color.[4]

Financial Assistance

Of the permissible uses of the Homeowner Assistance Fund as outlined in the Treasury guidance, HOPE recommends the following be prioritized:

- Mortgage payment assistance or reinstatement after forbearance delinquency, or default;

- Escrow payment assistance, including ;

- Homeowner’s insurance, mortgage insurance, and flood insurance ;

- Homeowner’s association, condominium association fees, or common charges;

- Property taxes;

- Principal reduction, including for second mortgages provided by a nonprofit or government entity;

- Interest rate reduction.

The other permissible uses, including assistance to cover utilities, internet service, and home repairs to maintain the habitability of a home or assistance to enable households to receive clear titles to their properties would also be helpful to homeowners if funds are available.

Documentation Requirements

HOPE fully supports Treasury’s guidance that state programs “should avoid establishing documentation requirements that are likely to be barriers to participation.”[5] Treasury allows programs to accept attestation of their financial hardship as well as for their income, in combination with geographic average income data, or individual supporting documentation. If the program chooses to require individual supporting documentation, those requirements should be as flexible as possible and not require duplicative documentation. Allowances for attestation should be described up front in application materials, rather than only made known to program participants who request it, or, as a last resort.

It is critical that the method of application be flexible and allow for options beyond online submission, including paper application and mobile phone uploads for documentation. Online submissions can be a significant barrier for some homeowners as has been demonstrated by recent Rental Assistance Programs.

Context for HOPE’s Recommendations

HOPE’s recommendations for the development of an equitable program is rooted in the organization’s own mortgage lending experiences and analysis of data on the disproportionate economic impact of COVID-19 on low-income communities and communities of color.

Mortgage lending is a key component of HOPE’s strategy to close the racial wealth gap in the Deep South. Over the last ten years, HOPE’s mortgage portfolio nearly quadrupled from nearly $34 million in 2010 to $127 million at the end of 2020. In 2020, 86% of HOPEs mortgage loans were made to people of color, primarily Black borrowers, and 83% were made to first time homebuyers. Importantly, the organization accomplished this growth through responsible lending as the organization finished the year with a mortgage charge off rate of fifteen basis points.

Since the beginning of the pandemic, over a quarter of HOPE’s mortgage borrowers were placed in forbearance at some point. For context, in June 2020, the national rate of mortgages in forbearance was 8.55%. Of the borrowers currently in forbearance at HOPE, more than a third have been in forbearance for more than 12 months.

In the coming months, the threat of foreclosure will create worry both for borrowers and lenders, as forbearance periods end and as borrowers still struggle to make ends meet. Whether the region, the industry, and mortgage borrowers are able to transition with the necessary resources and support will have significant impacts on the perseveration or loss of Black homeownership and the homes of those most affected by the pandemic.

[1] Sara Miller, “New Census Data on Employment Income Loss Underscore Magnitude of Financial Hardship in the Deep South from the Pandemic,” Hope Policy Institute, Aug. 19, 2020, http://hopepolicy.org/blog/new-census-data-on-employment-income-loss-underscores-magnitude-of-financial-hardship-in-the-deep-south-from-the-pandemic/

[2] Analysis of Bureau of Labor Statistics, Current Employment Statistics (State and Metro Area) and U.S. Department of Labor Office of Unemployment Insurance, UI Weekly Claims.

[3] U.S. Department of the Treasury, “Homeowner Assistance Fund Guidance”, April 14, 2021 p.6, available at https://home.treasury.gov/system/files/136/HAF-Guidance.pdf

[4] Partners for Rural Transformation, “Transforming Persistent Poverty in America: How Community Development Financial Institutions Drive Economic Opportunity,” Nov. 2019, https://www.ruraltransformation.org/wpcontent/uploads/2020/03/Transforming_Persistent_Poverty_in_America_-_Policy-Paper-PRT-_FINAL.pdf

[5] U.S. Department of the Treasury, “Homeowner Assistance Fund Guidance”, April 14, 2021, p.5 available at https://home.treasury.gov/system/files/136/HAF-Guidance.pdf

Share this article.