HOPE Submits Comment Calling for Racial Equity in New Markets Tax Credit Program

March 4th, 2021

March 1, 2021

Mr. Christopher Allison

NMTC Program Manager

CDFI Fund, US Department of the Treasury

1500 Pennsylvania Avenue NW

Washington, DC 20220

Via Electronic Transmission

nmtc@cdfi.treas.gov

RE: New Markets Tax Credit Program Allocation Application

FY 2021- FY2024 Funding Rounds

Response to Notice and Request for Public Comment

OMB Number: 1559-0016

To view a pdf of this comment click here.

Dear Mr. Allison:

Please find below the comments of the Hope Enterprise Corporation/ Hope Credit Union/Hope Policy Institute (HOPE) in response to the New Markets Tax Credit Program Allocation Application FY 2021-FY 2024 Funding Rounds Notice and Request for Public Comment dated December 29, 2020.

HOPE is a community development financial institution, credit union, loan fund and policy institute that provides affordable financial services; leverages private, public and philanthropic resources; and engages in policy analysis to fulfill its mission of strengthening communities, building assets, and improving lives in economically distressed areas throughout the Deep South.

HOPE was established to ensure that all people regardless of where they live, their gender, race or place of birth have the opportunity to support their families and realize the American Dream. Since 1994, HOPE has generated over $2.9 billion in financing that has benefitted more than 1.7 million people throughout Alabama, Arkansas, Louisiana, Mississippi and Tennessee.

Since the launch of the New Markets Tax Credit (NMTC) program in 2003, Hope Enterprise Corporation (HOPE) has had the opportunity to invest $212 million in NMTC financing in the communities we serve. Throughout the program, HOPE has advocated for innovative uses of NMTCs to best meet the needs of low-income communities and communities of color in the Deep South, both urban and rural.

HOPE was involved with the effort to create the program, working with Congress and the Clinton and Bush administrations during its passage and implementation. HOPE’s CEO, Bill Bynum was Chairman of the CDFI Fund Advisory Board from 2002-2012.1

After implementation, HOPE was instrumental in the removal of barriers so that nonprofit organizations could benefit from the NMTC structure and piloted the leverage loan structure that is widely used in the program today.

As a Minority-controlled Community Development Entity (CDE) and a designated Minority Depository Institution (MDI) by the National Credit Union Administration (NCUA), HOPE is well situated to provide not only financial services and make targeted investments in Black communities but also advocate for policies that will help close the racial wealth gap caused by generations of under investment and extraction.

The racial wealth gap is deep, and the economic and social benefits of closing it are vast. Ultimately, closing the racial wealth gap has the potential to increase the national Gross Domestic Product (GDP) between $1 and $1.5 trillion by 2028.2 Closing the gap in access to capital for people and communities of color and the institutions that serve them is a critical pathway to closing the racial wealth gap. New Markets Tax Credits are a powerful economic development tool that can be used to help close the gap.

Under consideration in this notice and request for public comment, is the NMTC program application used to collect data that once evaluated, will direct $25 billion in investment over the next five years in distressed communities. Relevant to this discussion is the way the application and scoring process and the resulting distribution of allocations can explicitly address or sustain the racial wealth gap that persists even among financial and community development institutions.

The importance of investing in Minority-led Community Development Entities

Research from the FDIC has shown that Minority Depository Institutions (MDIs) are a proven way to advance economic mobility in Black communities. MDIs are located in Black communities and serve their communities more equitably. An estimated six out of 10 people living in the service area of Black owned banks are Black, in contrast to six out of 100 for banks that are not Black-led. 3 Additionally, the study found that Black owned financial institutions originate a substantially higher proportion of mortgages and small business loans to Black borrowers than non-minority financial institutions.4

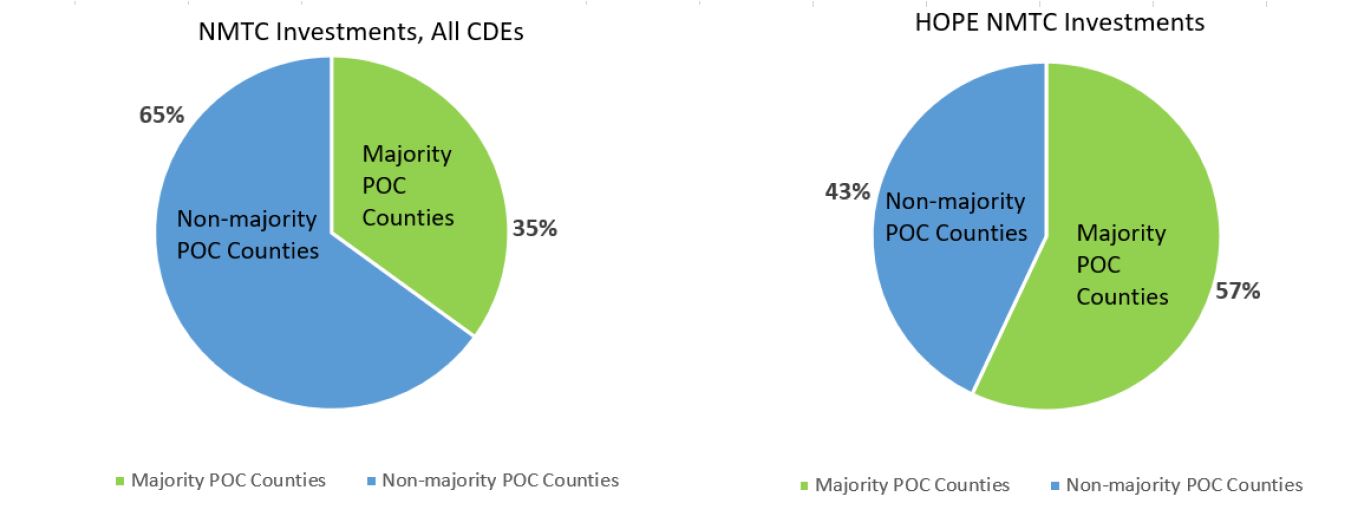

A majority (57%) of HOPE’s NMTC investments have been deployed in counties with a majority of residents who are people of color (see Figure 1). In contrast, only 35% of all NMTC investments have been deployed in majority people of color counties.

In addition to where investments are being made, it is important to look at the types of businesses being supported by NMTC investments. One specific way that the proposed NMTC application has collected data on who potential CDEs are serving is by showing the percent of their investments that go to Disadvantaged Businesses or Disadvantaged Communities. This analysis should remain a part of the NMTC application and the definition of Disadvantaged Businesses should not be changed as proposed to eliminate businesses that have inadequate access to investment capital. This is a key factor in evaluating a CDE’s experience deploying investments where they are needed most, especially for businesses led by people of color who are often the very ones facing underinvestment.

Figure 1: New Markets Tax Credit Investments in Majority People of Color Counties 2003-2017

Source: Hope Policy Institute analysis of data from the CDFI Fund NMTC Award and U.S. Census Bureau

Similarly, while changes are currently not proposed that would broaden the definition of Minority-owned or Minority-controlled CDEs, HOPE would be opposed to any recommendation that would include CDEs with less than 51% of minority equity ownership or board membership. The CDFI Fund should consider including measures in addition of ownership and governance that take into account an organization’s track record of serving communities of color. A recent example is of such a definition is the designation “minority lending institutions,” as included in the Consolidated Appropriations Act of 2021 which could be broadened to include activities of non-lender CDEs.

A “minority lending institution” is a CDFI where a majority of both the number and dollar volume of arm’s-length, on-balance sheet financial products of the CDFI are directed at minorities or majority minority census tracts or equivalents; and is (1) an MDI as defined by FDIC or NCUA or (2) meets other standards of accountability to minority populations as determined by the Fund.5

Allocations for Minority-led Community Development Entities represent a small portion of NMTC allocations overall

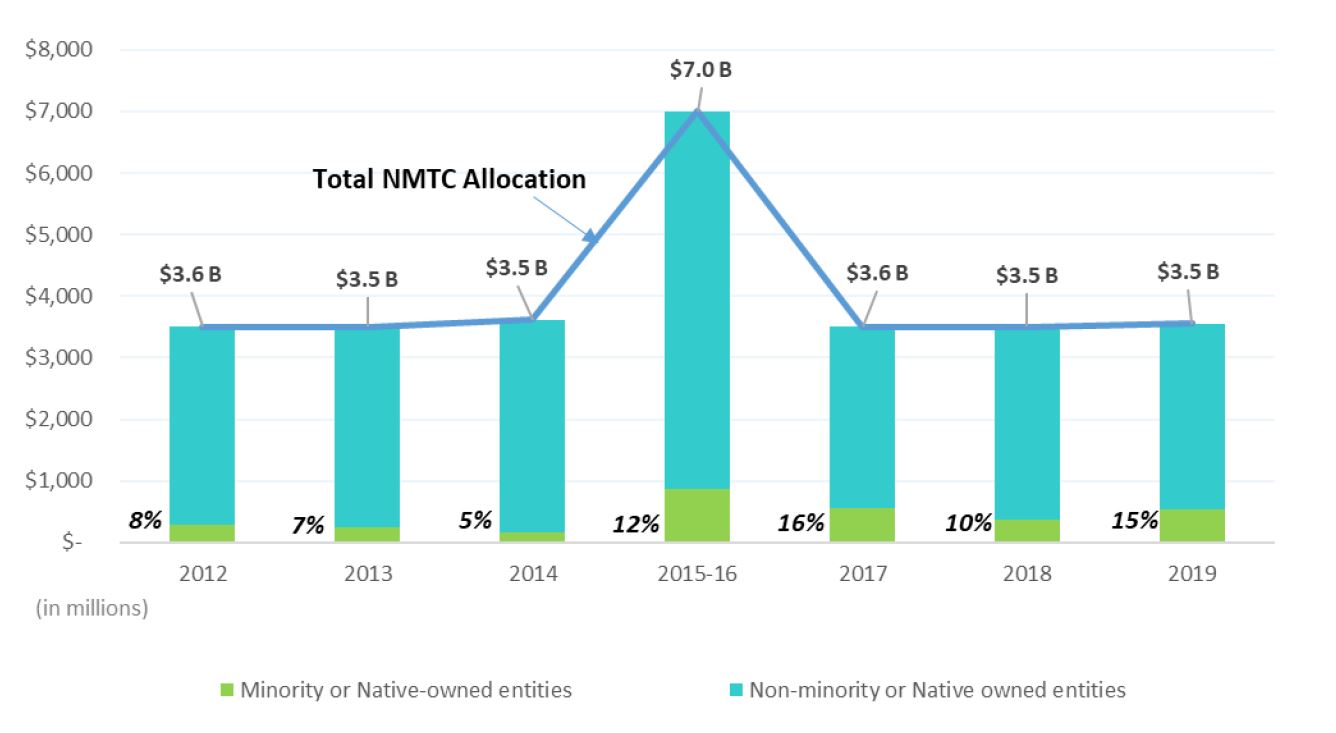

The benefits of a NMTC allocation go beyond the critical community investments deployed by CDEs in distressed areas. A NMTC allocation also provides an infusion of capital for the CDEs themselves that can then be the basis for other types of investments for years to come. This is especially important to Minority-led financial institutions and community development organizations that are undercapitalized compared with white-led institutions. This disparity can be seen by looking at CDFI Fund awardees. Persistently for every year in a 15 year span, the median asset size of white-owned CDFI Fund awardees has been at least twice the median asset size of Minority-owned awardees. In some years, it was 3 times as high.6 Similarly, racial disparities appear in the New Market Tax Credit Program. The chart below shows the percentage of NMTC allocations that have gone to Minority-owned or Minority-controlled CDEs over the last several years for which data was available. The percentage since 2012 has ranged from 5% in 2014 to 16% in 2017 and 15% in 2019 (Figure 2).

It is unclear if this is representational to the proportion of the number of Minority-owned or controlled CDEs because there is no comprehensive dataset of CDEs by ownership demographic. In either case, it is clear that white-owned CDEs are the significant majority of recipients of NMTC allocations even though Minority-owned or controlled financial institutions are often serving or located in communities with greater economic distress.

Figure 2: Share of NMTC Allocations Awarded to Minority-led Community Development Entities 2012-2019

Source: CDFI Fund, “NMTC Program Award Book” 2019, 2018, 2017, 2015-16, 2014, 2013, and 2012

Recommendations for Improving access for Minority-led CDEs

The NMTC program should work to remove barriers for Minority-led CDEs and implement measures that will explicitly encourage both greater success for Minority-led CDE applicants, particularly those with a long-track record of serving communities of color and now seeking to expand that impact via the NMTC program. To this end, HOPE recommends the following:

- Set aside a portion of NMTC allocation specifically for Minority-led Community Development Entities similar to the set aside for Rural CDEs. In conjunction with the development of a set aside, the definition of Minority-led CDEs should take into account an organization’s track record of serving communities of color like the designation “minority lending institutions,” as included in the Consolidated Appropriations Act of 2021 which could be broadened to include activities of non-lender CDEs.

- Cap the amount of allocation allowed for previous awardees to a certain amount over a 3-4 year period to allow the funds to be more equitably distributed across a range of CDEs particularly new entrants.

- Conduct an in-depth assessment of the NMTC program application and scoring areas that may be perpetuating racial disparities in choosing which CDEs receive an allocation and how much of an allocation they are awarded. For instance, the areas of the evaluation process that assesses an applicant’s experience with the NMTC program could inhibit the selection of new, Minority-led CDEs.

- Create incentives for experienced CDEs to work with new and/or Minority-led CDEs to gain NMTC experience.

- Provide consistent and detailed public data on Minority-led CDE certifications and awards for both CDE allocations and QLICIs, including whether a CDE is Minority-led on public CDE allocation data. Further, data should be provided on the number of Minority-led and white-led applicants, not just awardees. Current data on allocation awards to Minority-led CDEs is only available in aggregate in the narrative of the NMTC Program Award Book.

- Provide ongoing training and technical assistance to develop more Minority-led CDEs. In 2017, the CDFI Fund contracted with the National Community Investment Fund to provide a training and technical assistance program for Minority CDEs in order to develop more capacity among minority-led CDEs. This training program was a good start, but further efforts are needed.

The racial wealth gap is the result of systemic exploitation and extraction of the people and resources of a community. It is the result of centuries of policies such as slavery, land theft, and redlining, that have extracted and redistributed wealth and resources and contributed to generational poverty. The result of this extraction and exploitation can still be seen today as high unemployment, poor health outcomes, and lack of access to financial institutions7. The New Markets Tax Credit is an important tool that can help reverse this extraction. Its impact can be multiplied by increasing investments in Minority-led institutions.

Thank you for your consideration of this information. HOPE appreciates the opportunity to provide comments on the NMTC Program Allocation Application and the continued leadership of the CDFI Fund in deploying critical investments in distressed areas and foster economic growth in our communities.

Sincerely,

Kendra Key

Senior Vice President

Community and Economic Development

Sara Miller

Policy Analyst

1 https://files.consumerfinance.gov/f/201506_cfpb_bios_consumer-advisory-board.pdf

2 McKinsey and Company, “The economic impact of closing the racial wealth gap,” Aug. 13, 2019, https://www.mckinsey.com/industries/public-and-social-sector/our-insights/the-economic-impact-of-closing-the-racial-wealth-gap

3 Federal Deposit Insurance Corporation, “2019 Minority Depository Institutions: Structure, Performance, and Social Impact.” https://www.fdic.gov/regulations/resources/minority/2019-mdi-study/index.html

4 Ed Sivak, Hope Policy Institute “Minority Depository Institutions of the Deep South” Policy Matter Blog, July 15, 2020 http://hopepolicy.org/blog/minority-depository-institutions-in-the-deep-south/

5 Sec. 523(c)(4) of the Consolidated Appropriations Act of 2021

6 Kiyadh Burt, Hope Policy Institute, “Analyzing the CDFI Asset Gap: Examining Racial Disparities in CDFI Fund Awardees from 2003 to 2017,” November 5, 2020 available at http://hopepolicy.org/briefs/analyzing-the-cdfi-asset-gap-examining-racial-disparities-in-cdfi-fund-awardees-from-2003-to-2017-2/

7 Partners for Rural Transformation, “Transforming Persistent Poverty in America” March 2020 available at https://www.ruraltransformation.org/wp-content/uploads/2020/03/Transforming_Persistent_Poverty_in_America_-_Policy-Paper-PRT-_FINAL.pdf

Share this article.