New Report Charts Path for Ending Persistent Poverty in Rural America

December 3rd, 2019

Since 2014, HOPE has collaborated with several community development finance institutions (CDFIs) across the country to eradicate poverty in rural areas. This collaboration, known as Partners for Rural Transformation, is a coalition of six CDFIs located in and serving regions with a high prevalence of persistent poverty, which is any county that has experienced poverty rates of at least 20% for 30 years[1]. The partners are Community Development Corporation of Brownsville, Communities Unlimited, Fahe, First Nations Oweesta Corporation, Hope Enterprise Corporation/Hope Credit Union (HOPE), and Rural Community Assistance Corporation. Collectively, they serve significant swaths of rural communities throughout the nation — the Mississippi Delta, Appalachia, Indian Country, and communities along the U.S. / Mexico Border. The coalition is committed to providing affordable housing and sound financial products and services for rural communities, and has extensive expertise and accomplishments spanning multiple decades.

Persistent poverty is the result of systemic exploitation and extraction. Exploitative, state sanctioned policies such as slavery, land theft, and redlining, have served to redistribute wealth and resources from rural communities, contributing to generational poverty. These communities continue to struggle with the lasting impact of oppression and its associated ills e.g. high unemployment, poor health outcomes, and lack of access to financial institutions.

In a recently published report, Transforming Persistent Poverty in America: How Community Development Financial Institutions Drive Economic Opportunity, Partners for Rural Transformation find that persistent poverty counties lag behind national rates of unemployment, banking status, and health outcomes.

- 86% of persistent poverty counties have unemployment rates in excess of the national average;

- 75% of the counties in the country that have household unbanked/underbanked rates at 1.5 times the national average are persistent poverty counties;

- 81% of persistent poverty counties are in the bottom quartile of counties in terms of health outcomes; and

- Of the 395 persistent poverty counties, a “health-related drinking violation” occurred in approximately 42% of the counties – nearly five percentage points higher than the rate nationally.

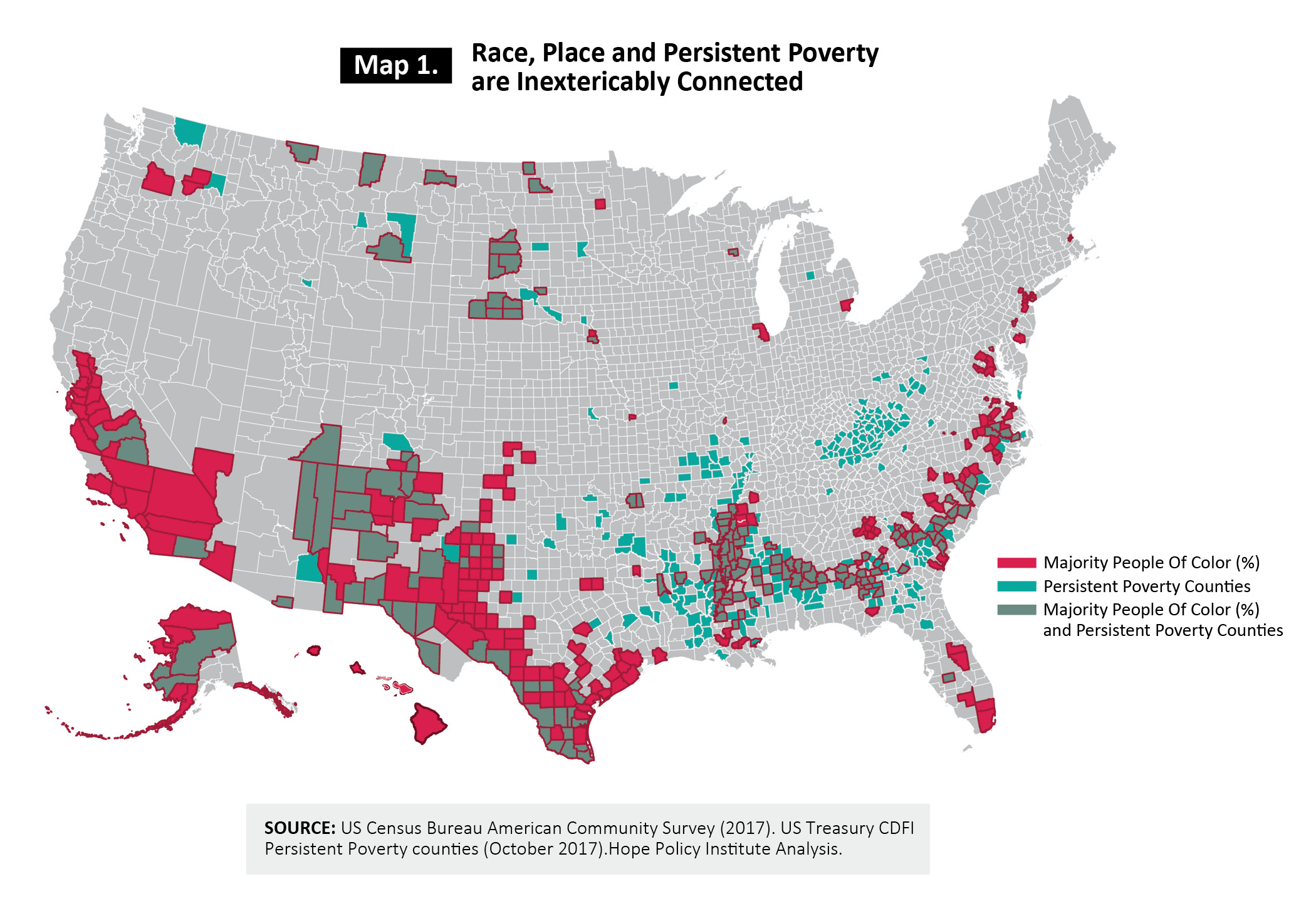

Furthermore, the report shows that people of color and rural communities comprise the majority of persistent poverty counties. Of the 395 persistent poverty counties shown, eight out of ten are non-metro {rural}, and the majority (60%) of people living in persistent poverty counties are people of color[2]. See Map 1.

Despite the concentration of poor economic indicators, investment has been lacking in these communities. The report highlights the low-level of philanthropic and capital investment compared with other regions of the county: “From 2010-2014, grant making in Appalachia, the Mississippi Delta and the Rio Grande Valley was around $50 per person – well behind the national average of $451 and $4,096 in San Francisco. Bank investment trails in poor rural areas as well. In 2017, only 27 cents of every dollar borrowed by rural CDFIs was from a bank. In contrast, over half the borrowed funds from urban CDFIs were supplied by banks.”

Given the challenges facing persistent poverty counties, Partners for Rural Transformation advocate for the following policy remedies:

- Balance Philanthropy’s Impact in Persistent Poverty Areas with other Parts of the Nation

- Create a $1 billion Persistent Opportunity Fund

- Increased Investment from National Community Development Intermediaries

- Expand Persistent Poverty Bank Lending and Community Development Investment

- Modernize CRA to require and incentivize persistent poverty investments

- Create incentives for bank investment into CDFIs located in and with long track records of serving rural persistent poverty regions.

- Increase and Prioritize Federal Investment in Persistent Poverty Places

- Establish floors for federal discretionary spending of at least 10% in persistent poverty areas

- Rectify inequitable income eligibility criterion so that rural communities can better participate in community development programs

- Advance a Persistent Poverty Research Agenda

To read the full report, click here. Follow the conversation on social media at #PowerofRural

References

U.S. Treasury Community Development Financial Institutions Fund. https://www.cdfifund.gov/Documents/PPC%20updated%20Oct.2017.xlsx. (Accessed November 19, 2019).

Partners for Rural Transformation. 2019. “Transforming Persistent Poverty in America: How Community Development Financial Institutions Drive Economic Opportunity”. https://fahe.org/wp-content/uploads/Partners-for-Rural-Transformation-DRAFT.pdf

[1] U.S. Treasury Community Development Financial Institutions Fund. https://www.cdfifund.gov/Documents/PPC%20updated%20Oct.2017.xlsx. (Accessed November 19, 2019).

[2] There are 473 persistent poverty counties, including Puerto Rico. Puerto Rico is not shown due to mapping limitations; therefore, only 395 persistent poverty counties are shown.

Share this article.