New Report Reveals Many Mississippians are in Financial Limbo

August 3rd, 2017

Mississippi households, and more broadly, Mid South households, continue to struggle in low-wage jobs that do not allow them to save for a more prosperous future. The 2017 Prosperity Now Scorecard (formerly the Assets & Opportunity Scorecard) reveals that the lack of quality job opportunities in the state makes it harder for families to meet basic expenses—and nearly impossible to save enough to move up the economic ladder. More than half (53.4%) of Mississippi households do not have enough savings to weather the storm of a significant financial hardship, like a job loss, for more than three months. The new data, released in the Prosperity Now Scorecard, underscore the need for investments in high-poverty areas that create quality jobs as well as quality financial services that help support better opportunity for households who live in underserved communities.

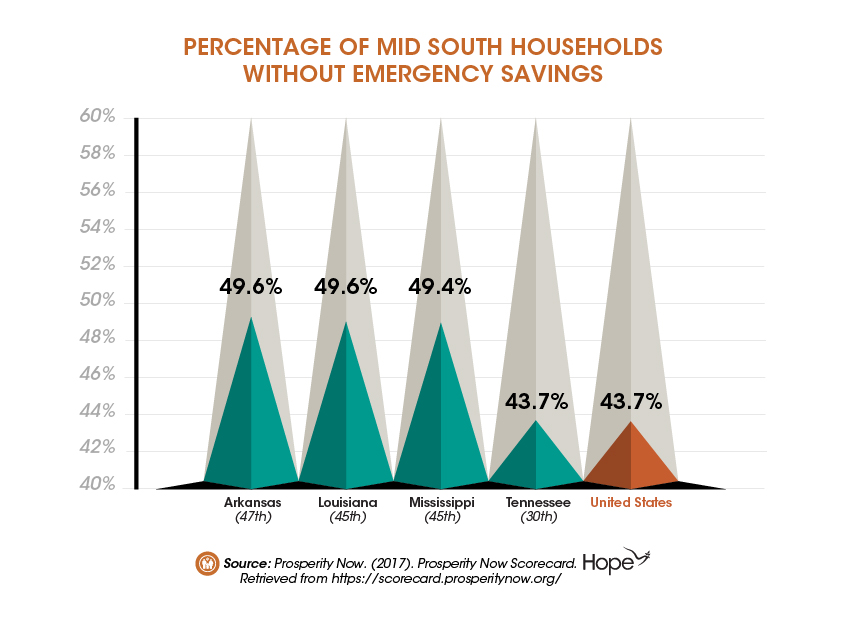

The Scorecard findings illustrate that Mississippi households are among the most financially vulnerable. Almost half (49.4%) of Mississippi households did not set aside any savings for emergencies in the past year – the sixth highest rate in the nation and higher than the national rate of 43.7 percent (See Chart). Oftentimes, these households lack the flexibility to invest in wealth-building tools, such as a home or post-secondary education, because they are not connected to affordable, quality financial services.

Click to enlarge

Mississippi households of color face even greater obstacles. They are more than twice as likely to live below the poverty line as white households (33.2% compared to 13.0%) and much less likely to own a home or other assets that boost long-term financial stability. More than half of households of color (53.2%) in the state own homes, compared to 76.5 percent of white, non-Hispanic households.

There is much work to be done to help lift Mississippians and other Mid South residents out of poverty, particularly in high-poverty areas. Community Development Financial Institutions (CDFIs) and Community Development Credit Unions (CDCUs), like Hope, continually work to meet the needs of historically underserved populations. It is imperative to expand support and invest in CDFIs and CDCUs to create ladders of opportunities in these communities.

Hope Policy Institute will continue to share data from the 2017 Prosperity Now Scorecard and highlight policy options for building assets among low-wealth households.

Source:

Prosperity Now. (2017). Prosperity Now Scorecard. Retrieved from https://scorecard.prosperitynow.org/

Share this article.