Tax Expenditure Series Part 1: What is a Tax Expenditure?

May 24th, 2011

A new report by the Center on Budget and Policy Priorities (CBPP) examines the role that Tax Expenditure Reports play in the improvement of state budget accountability and evaluates state Tax Expenditure Report practices. Tax Expenditures are exceptions to the general tax code, like deductions, exemptions, and credits, that reduce state revenue. Like state programs, they are often enacted for a public purpose like promoting economic development or reducing the costs of caring for children. However, unlike other types of state spending, they are not subject to regular review or budget constraints.

Once enacted, tax expenditures are not subject to annual scrutiny through the appropriation process. Not only are tax expenditures not subject to regular review, but they are also not limited to a total dollar amount, like direct state spending. The CBPP report provides one example of a tax expenditure that cost a state 10,000 percent more than was estimated.

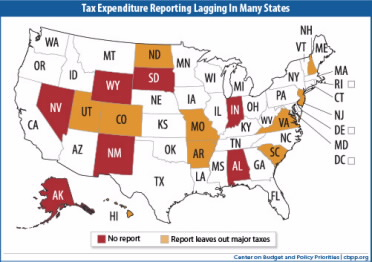

In order to provide some regular review and cost estimates, most states (44 total) compile a Tax Expenditure Report that provides data on the purpose and cost of each tax expenditure. Mississippi law requires an annual Tax Expenditure Report that is prepared by the Institutions of Higher Learning Center for Policy Research and Planning. It provides information including some cost estimates on the state’s tax expenditures. Mississippi’s report meets many of the criteria set forth by the CBPP but can still improve in many ways.

Click to enlarge

Over the course of the week, we will provide a snapshot of Mississippi’s tax expenditures and offer recommendations for how the Mississippi Tax Expenditure Report could be enhanced. Stay tuned for:

Part 2: What Tax Expenditures look like in Mississippi

Part 3: How Mississippi’s Tax Expenditure Report could be improved

Share this article.