Tax Expenditure Series Part 2: How Much Does Mississippi Spend on Tax Expenditures?

May 25th, 2011

As we discussed in Part 1 of the tax expenditure series, tax expenditures are exceptions to the general tax code, like deductions, exemptions, and credits, that reduce state revenue. Like state programs, they are often enacted for a public purpose like promoting economic development or reducing the costs of caring for children. However, unlike other types of state spending, they are not subject to regular review or budget constraints.

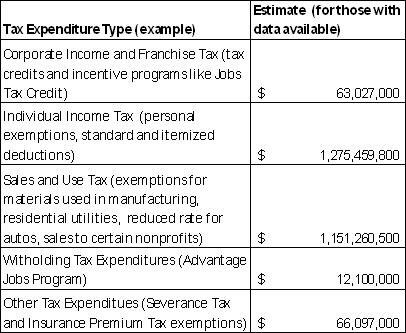

The annual Tax Expenditure Report provides data on most of the state’s tax expenditures. The table below sums the estimates provided in the state report by tax source and lists some examples of each type of tax expenditure. It is provided here for reference only and should not be considered a comprehensive look at how much tax expenditures are costing the state. It does not include 27 tax expenditures for which insufficient data is available to provide an estimate.

Click to enlarge

Tax Expenditure Estimates by Type, FY 2011

The estimates provided above total more than $2.5 billion, however, total tax expenditures are likely greater. Some of the areas for which there are no data in the report include all corporate income tax deductions, installment loan tax exemptions, auto privilege tax exemptions, and a few sales tax exemptions.

By listing the tax expenditures by type in Mississippi, one should note that this post does not advocate for or against tax expenditures. The most important takeaway is that information on tax expenditures is often less transparent than information about appropriations, resulting in programs that are less accountable to taxpayers.

In some cases, the state does not report on the effectiveness of expenditures that cost millions of dollars (e.g., there is no public record of the number of jobs supported by the Jobs Tax Credit) or how much certain expenditures cost.

Tomorrow, we wrap up our tax expenditure series by focusing on how Mississippi’s report can be improved to make tax expenditures more transparent and accountable.

Source:

The Annual Tax Expenditure Report, Institutions of Higher Learning Center for Policy Research and Planning, November 2010.

Share this article.