The State of Student Debt

February 19th, 2016

For many adults in search of a high-paying job and benefits, a college degree is the ticket to the skills and experience they need. Four-year college graduates have more employment opportunities, higher earning potential, and better wages and benefits packages that help support individuals and families in becoming more economically secure. However, this security often comes at a price—plus interest: rapidly increasing tuition prompts many to take on student loans to finance their educations, leaving recent graduates—nationally and in the Mid South—saddled with student debt.

Average student debt varies significantly state by state and depending on the type of institution attended; community college attendees typically borrow less than students attending 4-year public or private nonprofit institutions and students at 4-year for-profit colleges generally take on the most debt.

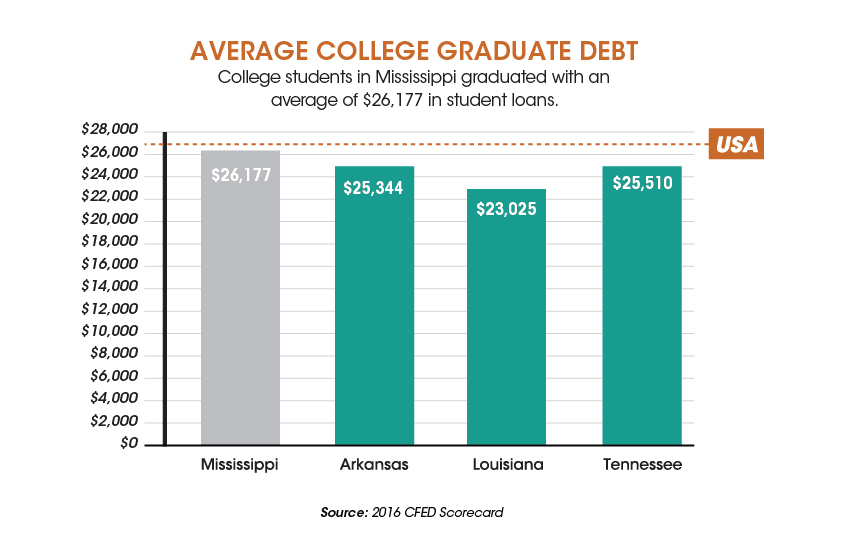

In the Mid South, the average college graduate amasses $25,014 in student loans, ranging from $23,025 in Louisiana to $26,177 in Mississippi, just shy of the $27,022 national average. This hefty price tag isn’t a fluke—graduating with debt is now the norm as more than half of Mid South college graduates walk across the stage with some degree of student debt.

While average student debt in Mid South states is below the national average, the impact of accumulating large sums of debt is the same. Significant student debt limits financial resources available to build assets. When a considerable portion of monthly earnings is automatically earmarked for loan repayment, young student debtors are unable to invest those earnings elsewhere. This means large, economy-driving purchases like new cars and homes are postponed along with contributing to savings or retirement.

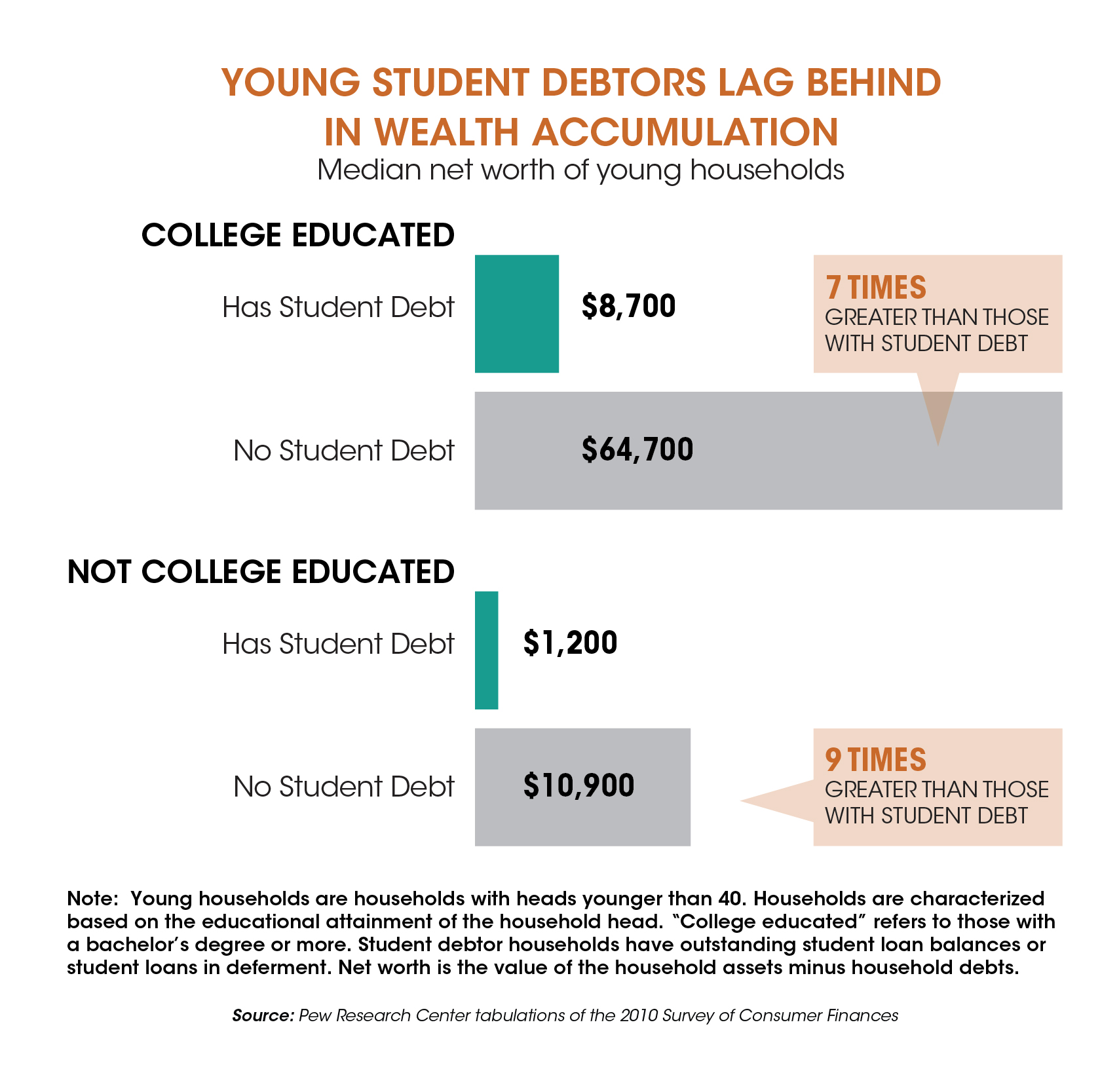

The wealth disparity between those with student debt and those without is another cause for concern: households headed by a young, college-educated adult without student debt have seven times the net worth of households headed by a young, college-educated adult with student debt. In these cases, the same tool intended to help increase economic security is preventing some college graduates from achieving it.

In many ways, student loans are a necessary evil, but there are ways to mitigate the debt burden on college graduates. Giving students options to finance their education is essential to keep college affordable and debt under control. At the individual level, state aid programs like the Mississippi Tuition Assistance Grant (MTAG) help students afford college and minimize the need for loans while work-study allows students to work off tuition costs while enrolled. At the state level, slashed funding for public higher education institutions compels schools to raise tuition to cover costs. Maintaining funding levels for public universities and colleges in the legislature prevents the cost burden from being passed to students and reduces their need to take on loans, preserving higher education as an accessible, affordable pathway to economic security.

Share this article.