Understanding the Payday Loan Debt Trap

January 13th, 2011

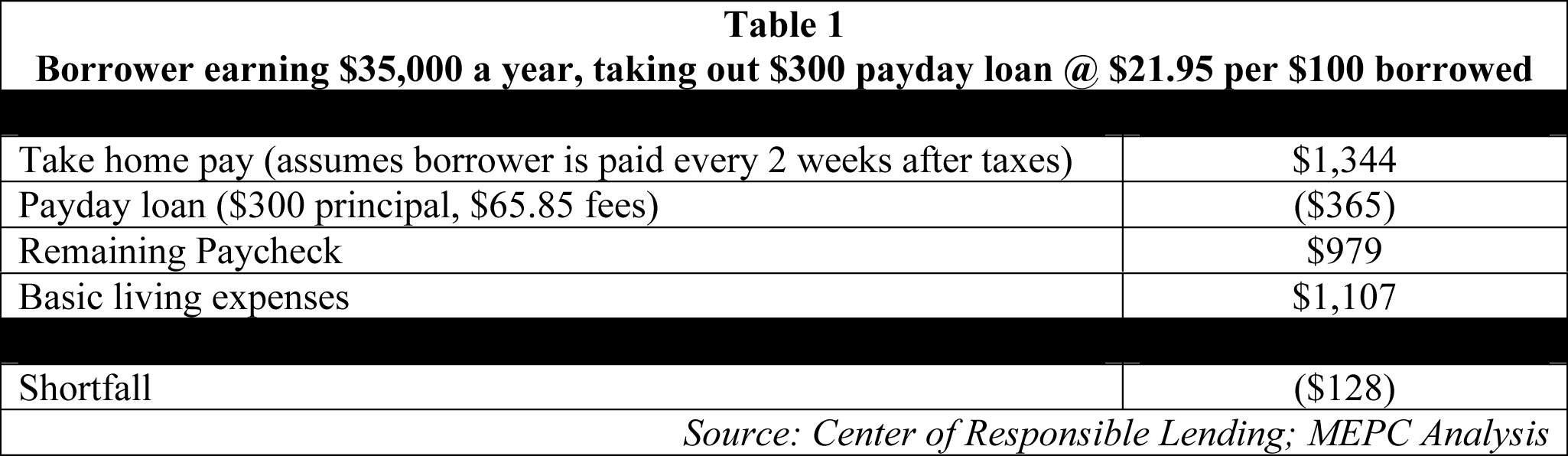

Once a borrower takes out a payday loan, he or she could quickly find themselves in a situation where they need multiple payday loans to cover expenses. Table 1 illustrates how a family could find themselves caught in the debt trap. A family earning $35,000 a year receives approximately $1,344 every two weeks in take home pay. After taking out a payday loan and repaying it with fees for a total of $365, the family has only $979 left to cover $1,107 in expenses.

Click to enlarge

Still short, the family will either need to take out another payday loan or choose to skip paying certain bills. On average, borrowers take out eight payday loans per year. A 36 percent rate cap in Mississippi with 90 days for repayment would allow working families to avoid the debt trap.