FDIC Survey: Banks Efforts to Integrate the Underserved Into the Financial Mainstream

December 27th, 2012

This month, the Federal Deposit Insurance Corporation (FDIC) released the results of the 2011 FDIC Survey of Banks’ Efforts to Serve the Unbanked and Underbanked, which assesses insured depository institutions’ efforts to integrate unbanked and underbanked consumers into the financial mainstream. Essentially, the primary purpose of the Bank Survey is to better understand the efforts undertaken by the retail banking industry to provide financial products and services to underserved consumers. The Bank Survey is a complement to the2011 FDIC National Survey of Unbanked and Underbanked Households, which revealed that one in four households are either unbanked or underbanked. Unlike the Household Survey, the Bank Survey response was reported in aggregate form and not available by state.

Key Findings

Product Development, Marketing, and Advertising

Four out of ten banks (43 percent) developed and marketed specialized products, services, or programs for unbanked and underbanked consumers. Likewise, banks identified community outreach collaborations (39 percent) as the most effective marketing channel and automated telephone banking (62 percent) as the most effective retail strategy to reach underserved consumers.

Basic Financial Products and Services

Nearly half of all banks (42 percent) required an initial deposit of $100 to open a basic checking account, while 6 percent of banks required a minimum opening balance of more than $100. Forty-eight percent of banks required $50 or less to open an account.

Auxiliary Products

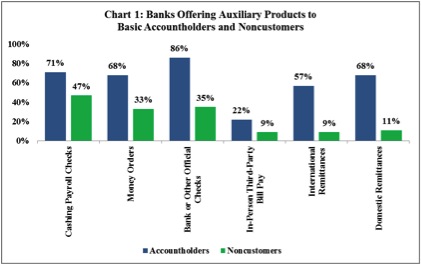

The most commonly offered auxiliary products to account holders and non-customers were payroll check cashing (71 percent for account holders and 47 percent for non-customers), bank or other official checks (86 percent for account holders and 35 percent for non-customers), and money orders (68 percent for account holders and 33 percent for non-customers). See Chart 1.

Financial Education and Outreach

Eight out of ten banks (81 percent) provided free counseling to underserved consumers. Fifty-eight percent of banks who offered free counseling rated it as either “very effective” or “effective.” Other financial education and outreach activities included teaching basic financial education (48 percent), funding community partners (51 percent), and providing technical expertise (56 percent).

Challenges in Offering Financial Products and Services to Underserved Consumers

Thirty percent of banks reported that consumers’ lack of understanding of financial products and services was a major challenge. Six percent of banks reported a lack of familiarity with financial or banking needs of underserved consumers, 12 percent reported developing products to meet the needs of the underserved, 19 percent reported effectively marketing products to the underserved, and 18 percent reported a lack of consumer demands as challenges in serving the unbanked and underbanked.

The Bank Survey emphasizes the need to implement policies that expand access to mainstream financial services and meet the needs of unbanked and underbanked consumers through financial inclusion. Banks provide consumers with the opportunity to save, borrow, and invest through safe and affordable banking practices. As such, people who are fully integrated into the financial mainstream have a solid foundation to save and build wealth and create a financially sound future for not only themselves but the nation’s economy. Policy opportunities that promote financial inclusion include expanding support for community development financial institutions and community development credit unions, both of which continuously work to provide financial opportunities to historically underserved populations.

A follow-up blog will focus on opportunities identified by the FDIC to expand access to mainstream financial services.

Source:FDIC, 2011 FDIC Survey of Banks’ Efforts to Serve the Unbanked

Share this article.