Key Designations in New PPP Increase Access for Small Businesses

January 26th, 2021

By Kiyadh Burt, Policy Analyst

Congress recently passed the Consolidated Appropriations Act, 2021 which injected $284 billion into the Paycheck Protection Program (PPP) for another round of funding to small businesses impacted by the pandemic.[1] The Paycheck Protection Program is a critical opportunity for businesses to receive capital to stay afloat during the pandemic yet many small businesses have faced challenges with accessing relief. This round of PPP was designed to address some of the shortcomings of previous rounds of funding and increase access for small businesses, minority-owned businesses, and the communities hardest by the pandemic.

Small businesses of color struggled to access relief during the first round of PPP.[2] Minority-owned businesses often lacked access to mainstream financial institutions like banks, which represented the majority of PPP lenders.[3] In addition, over 90% of minority-owned businesses were sole proprietors or self-employed. Sole proprietors were not initially eligible for PPP and by the time they could receive PPP relief, the funds had been mostly allocated.[4]

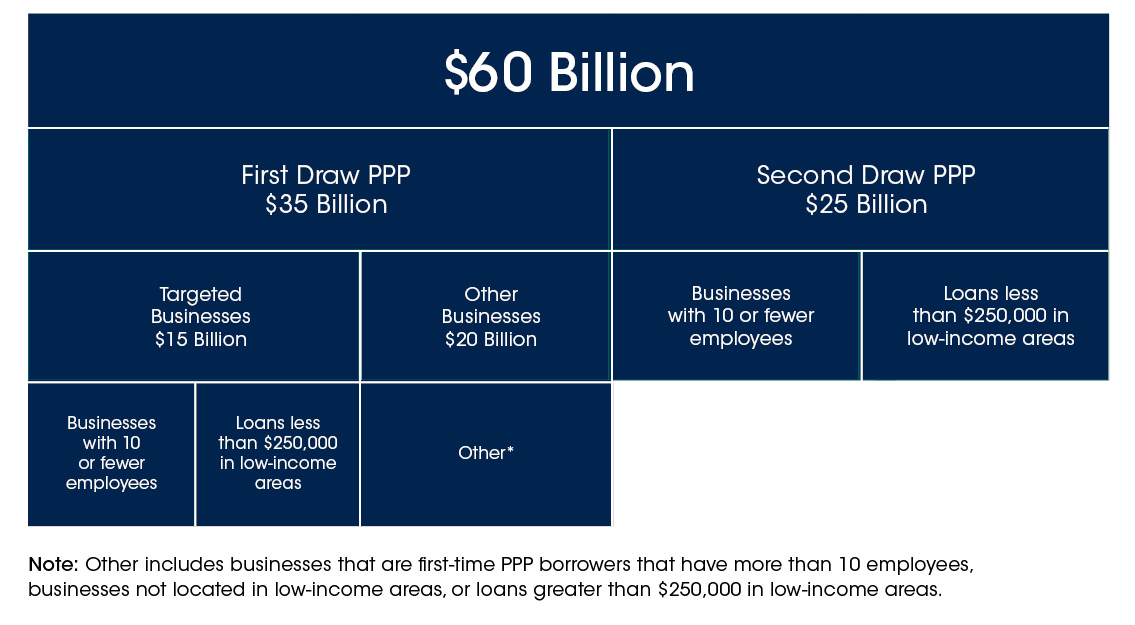

In this round of funding, an allocation of at least $60 billion has been reserved for small businesses most in need of relief. Over half ($35 million) of the $60 billion is reserved for first-time borrowers, $15 billion of which is designated for smaller, first-time borrowers with 10 or fewer employees, or loans less than $250,000 in low-income areas. For second draw PPP loans, $25 billion is reserved for smaller borrowers with 10 or fewer employees, or loans less than $250,000 in low-income areas. See graphic below.

Key PPP Designations for Disadvantaged Businesses

Small businesses will still be able to draw from the remaining funds in the program even after these funds are deployed. PPP funds are administered on a first come first served basis so this allocation is a critical development to ensure the smallest businesses have time to apply for and receive relief.

There is also a $15 billion designation for live venues, theatres, and cultural institutions such as museums which were severely impacted by shutdowns mandated by health regulations in response to the pandemic.

Community lenders such as Community Development Financial Institutions (CDFIs) and Minority Depository Institutions (MDIs) have a $15 billion designation to offer loans to small businesses. Community Development Financial Institutions are banks, credit unions, loan funds, or venture funds that are committed to increasing financial access to underserved communities and have received CDFI accreditation by the U.S. Department of Treasury’s CDFI Fund. Minority Depository Institutions are banks and credit unions that are owned or led by people of color. CDFIs and MDIs have a well-documented track record of serving small businesses and businesses of color that are overlooked by mainstream financial institutions. For example, in the last round of PPP funding CDFIs and MDIs nationally made over $16 billion in PPP loans with an average size of $74,000.[5]

In addition to the designations or set asides, the SBA only accepted PPP loans submitted through community lenders such as Community Development Financial Institutions and Minority Depository Institutions for the first two days of the program, January 11th and January 12. This priority access was a recognition by SBA of the role CDFIs, MDIs, and community lenders play in reaching smaller businesses and businesses of color. Although the window has passed, community lenders still have the $15 billon set aside to assist small businesses and businesses of color. Banks with less than $1 billion were able to process PPP loans that Friday, and all lenders had access to the PPP portal the next Monday. In the first week the PPP program, approximately 60,000 loans were deployed totaling over $5 billion.[6]

There were other important developments to the PPP that will increase benefits for PPP borrowers. First, businesses that received an Economic Injury Disaster Loan (EIDL) will be able to have their entire PPP loan forgiven. Prior to this legislation, the amount of the PPP loan to be forgiven was to be reduced by the amount of the EIDL. Second, PPP recipients will not have to pay taxes on their PPP loan. Additionally, PPP recipients will now have a greater time-frame to spend PPP funds, 24 weeks instead of 8, and can use funds to cover expenses to adhere to pandemic health regulations like purchasing plastic or glass separators or PPE. Finally, the federal relief package dramatically streamlines and reduces barriers to loan forgiveness for loans under $150,000.

With these changes to PPP, Congress and the SBA have made an effort to increase access for small businesses of color. Many small businesses faced systemic challenges to access PPP last year; yet, CDFIs and MDIs provided significant relief to businesses that would have otherwise been unserved. HOPE, like many other CDFIs, stepped up to meet the challenges facing businesses hardest hit to support the deployment of PPP funds. For the two states with the largest Black populations in the country, MS and LA, CDFIs made 7 times more PPP loans under $150,000 in than the five largest banks in the country combined (32,294 made by CDFIs vs 4,670 made by Chase, Bank of America, Wells Fargo, Citibank and U.S. Bank).

As of September 15, 2020, HOPE has funded 2,587 loans totaling $81 million, supporting more than 10,200 jobs in the Deep South. The majority of HOPE’s PPP borrowers are businesses owned or led by people of color and women, and the majority are located in communities of color. We will continue to provide access for businesses hardest hit with the new round of PPP funding, and advocate for policies that work for small businesses in the Deep South.

[1] Consolidated Appropriations Act, 2021, H.R. 133, 116th Congress. (2020).

[2] Kiyadh Burt, Hope Policy Institute, “CDFIs and MDIs Continue to Cater to Small Businesses Despite PPP Barriers,” July 23, 2020, http://hopepolicy.org/blog/cdfis-and-mdis-continue-to-cater-to-small-businesses-despite-ppp-barriers/

[3] Small Business Administration. (2020). “Paycheck Protection Program (PPP) Report”. https://www.sba.gov/sites/default/files/2020-08/PPP_Report%20-%202020-08-10-508.pdf

[4] Center for Responsible Lending. (2020). “The Paycheck Protection Program Continues to be Disadvantageous to Smaller Businesses, Especially Businesses Owned by People of Color and the Self-Employed”. April 6, 2020. https://www.responsiblelending.org/sites/default/files/nodes/files/research-publication/crl-cares-act2-smallbusiness-apr2020.pdf?mod=article_inline.

[5] Small Business Administration. (2021). “Paycheck Protection Program (PPP): Guidance on Accessing Capital for Minority, Underserved, Veteran and Women-Owned Business Concern”. https://www.sba.gov/sites/default/files/2021-01/Guidance%20on%20Accessing%20Capital%20for%20Underserved-508.pdf?utm_medium=email&utm_source=govdelivery

[6] Small Business Administration. (2021) “60,000 Paycheck Payment Protection Program Loans Approved in First Week”. https://www.sba.gov/article/2021/jan/19/60000-paycheck-protection-program-loans-approved-first-week

Share this article.